For further insights and opinions on this article, please contact the author:Chen Xun, Investment Department II, Nanjing Innovation Investment GroupEmail: chenx@njicg.com

Hydrogen energy is regarded as the energy of the future. As a type of secondary energy, it boasts an energy density as high as 142 MJ/kg, about three times that of gasoline, 3.9 times that of alcohol, and 4.5 times that of coke. Through fuel cells, it can achieve a comprehensive conversion efficiency of more than 90%. It is also a clean energy source: whether hydrogen is burned or undergoes electrochemical reactions in fuel cells, the only product is water, without pollutants or carbon emissions generated by traditional energy use. In addition, hydrogen production via water electrolysis using wind and solar power can solve the problem of abandoned wind and solar power, enabling green hydrogen to play an important role in the new-type power system dominated by renewable energy.

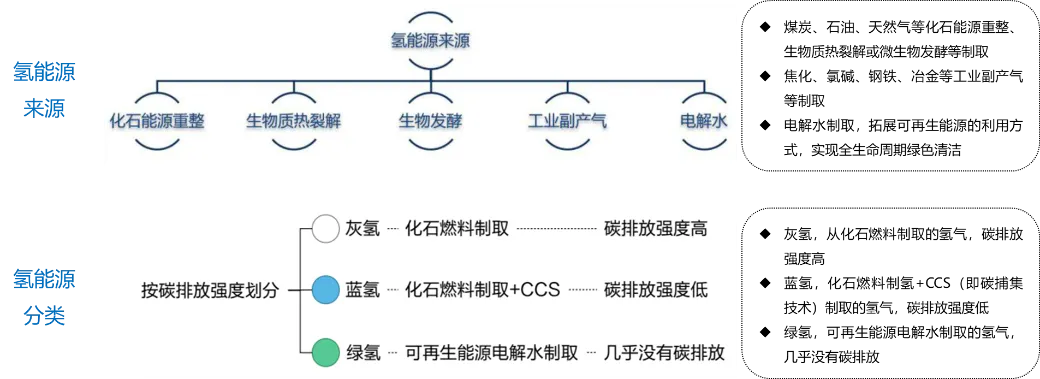

Sources and Classification of Hydrogen Energy

Hydrogen Energy is Moving Beyond the “Concept Stage”

Over the past few years, the hydrogen energy industry has become one of the most controversial sectors in new energy. On the one hand, it has been repeatedly included in national medium- and long-term plans and listed as a “future industry” alongside quantum technology and nuclear fusion. On the other hand, the industrial side has long been labeled as “many demonstrations, low profitability, and slow commercialization.”

Relevant Policies for China’s Hydrogen Energy Industry

In 2019, hydrogenation and other infrastructure construction were first mentioned in China’s Government Work Report. In October of the same year, the National Energy Commission held a meeting to accelerate the exploration of commercialization paths for hydrogen energy.In April 2020, the National Energy Administration issued the Energy Law of the People’s Republic of China (Draft for Comment), formally incorporating hydrogen energy into China’s energy development framework.In 2022, the Medium- and Long-Term Plan for the Development of the Hydrogen Energy Industry (2021–2035) was released.In October 2025, the Fourth Plenary Session of the 20th Central Committee of the Communist Party of China adopted the Recommendations of the Central Committee of the Communist Party of China on Formulating the 15th Five-Year Plan for Economic and Social Development, which proposed to “look ahead in laying out future industries… and promote quantum technology, bio-manufacturing, hydrogen energy and nuclear fusion, brain-computer interfaces, embodied intelligence, and 6G mobile communication to become new growth engines.”

From a longer-term perspective, the question for hydrogen energy is not “whether to develop it,” but “at what stage and in what way to develop it.” As the “dual carbon” goals enter the mid-term implementation phase and the energy structure transition deepens, hydrogen energy is gradually moving beyond the early policy concept stage into a more realistic and complex phase of industrial evolution.

The Original Intention of Developing the Hydrogen Energy Industry

In the new energy system, wind and solar power address power generation, lithium batteries address short-cycle energy storage, while hydrogen energy solves a more fundamental and difficult problem: how the energy system can achieve deep decarbonization across time, regions, and industries under a high proportion of renewable energy.

In sectors such as steel, chemicals, refining, long-distance transportation, and shipping, electrification alone cannot achieve carbon neutrality. These sectors either consume massive energy, rely on fossil fuels for processes, or have extremely high requirements for energy density and endurance. Hydrogen is currently one of the few energy sources that can provide feasible solutions in these scenarios.

This is why hydrogen energy is repeatedly emphasized for its systemic value in China’s 14th and 15th Five-Year Plans, as well as in the energy transition strategies of the EU, the U.S., and Japan: it is not a single-point technological breakthrough, but a key driver in the upgrading of the energy system.

From “Demonstration” to “System”: The Real Progress of the Hydrogen Industry

Reviewing the development trajectory over the past five years, China’s hydrogen energy industry shows clear phased features: policy leadership, demonstration-driven, and gradual formation of the industrial chain.

In the early stage of the 14th Five-Year Plan, the core policy goal was not immediate commercialization, but verifying technical routes, connecting the industrial chain, and cultivating market players through demonstration projects. As a result, numerous hydrogen projects were concentrated in fuel cell vehicle demonstration city clusters, water electrolysis hydrogen production demonstration projects, and park-level integrated energy projects.

Although these projects have difficulty generating considerable profits in the short term, their significance lies in moving a technical system that once existed only in laboratories and papers into engineering and industrialization.

The Hydrogen Industry is at an Inflection Point Before Industrial Innovation and Takeoff

This phase has indeed yielded results. The domestic substitution rate of electrolyzers, fuel cell stacks, key materials and components has increased significantly. Relatively clear industrial division has gradually taken shape in hydrogen production, storage, transportation, and application, and corporate capabilities have begun to differentiate. Meanwhile, China’s hydrogen industry has advanced to the forefront globally:

In 2024, the global production and consumption of hydrogen reached about 105 million tons, corresponding to a market size of approximately $150 billion.

As the world’s largest hydrogen consumer, China had a hydrogen capacity of about 50 million tons/year and output of about 37 million tons in 2024, with a domestic hydrogen market size of roughly 400 billion yuan.

Cost: An Inevitable Core Issue

All discussions about hydrogen energy ultimately return to one practical question: cost.

In the current industrial structure, hydrogen production is still dominated by fossil fuels (accounting for more than 50%), while green hydrogen accounts for less than 1%. Even in green hydrogen projects, the combined costs of electricity, electrolyzer equipment, storage and transportation, and refueling remain significantly higher than traditional gray hydrogen.

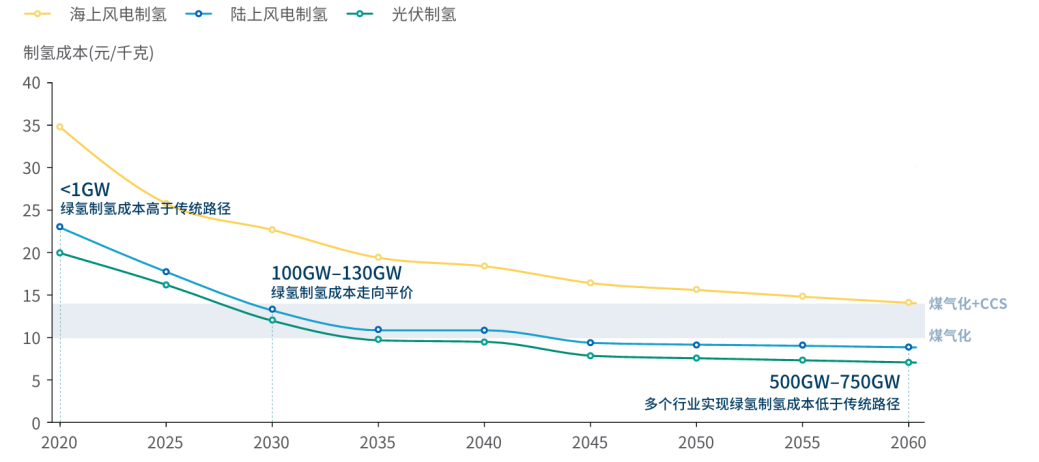

Notably, the cost structure is not static. Over the past three years, with the continuous decline in the levelized cost of wind and solar power and the sharp drop in electrolyzer prices, the marginal cost of green hydrogen has improved rapidly. Many research institutions predict that around 2030, with installed capacity expanding to over 100 GW, green hydrogen costs in regions with favorable renewable energy resources are expected to drop to 15 yuan/kg, approaching or even below the comprehensive cost of “coal-to-hydrogen + carbon capture.”

However, the real constraint on large-scale green hydrogen development is not a technical bottleneck in a single link, but insufficient coordination among production, storage, transportation, and application. While costs at the hydrogen production end are falling, midstream storage and transportation and end-use costs remain high, meaning overall economic viability is not yet fully achieved.

For example, in northwest regions rich in wind and solar resources (such as Inner Mongolia and Xinjiang), green hydrogen can be produced at very low electricity prices (below 0.2 yuan/kWh), with local production costs already in the range of 18–20 yuan/kg. Yet major consumer markets (such as the Yangtze River Delta and Pearl River Delta) are thousands of kilometers away, making high-pressure trailer and liquid hydrogen transportation costs prohibitive.

Hydrogen Energy Is More Than “Hydrogen Fuel Cell Vehicles”

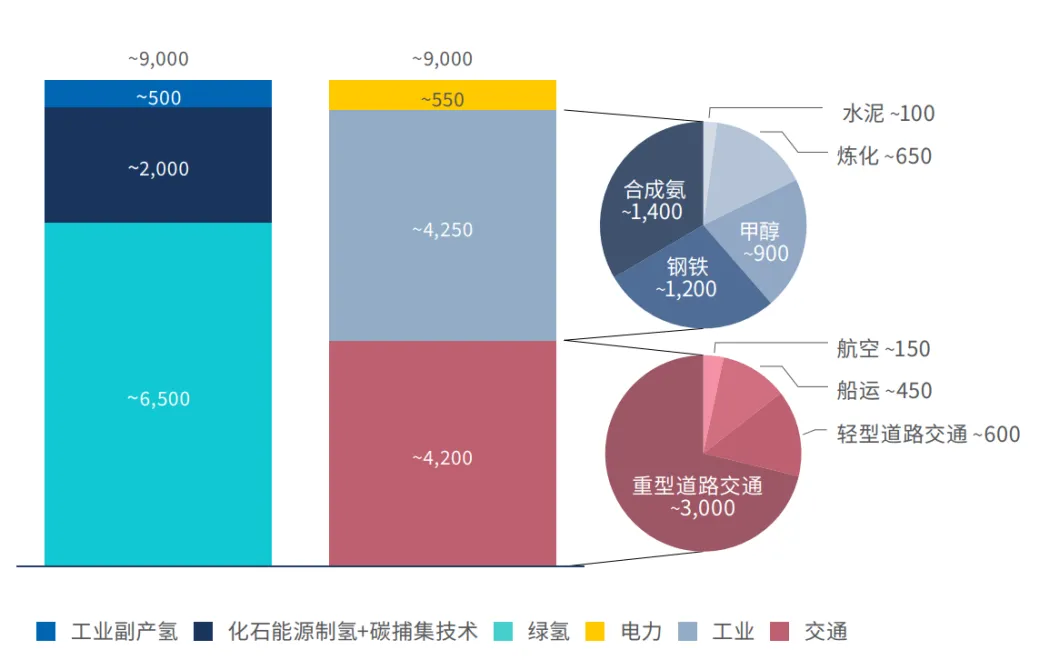

According to the China Hydrogen Energy Development Report 2025, industrial scenarios including synthetic ammonia, synthetic methanol, refining, coal chemical, and metallurgy accounted for more than 80% of hydrogen consumption in 2024, with the rest in transportation, power, and other sectors.

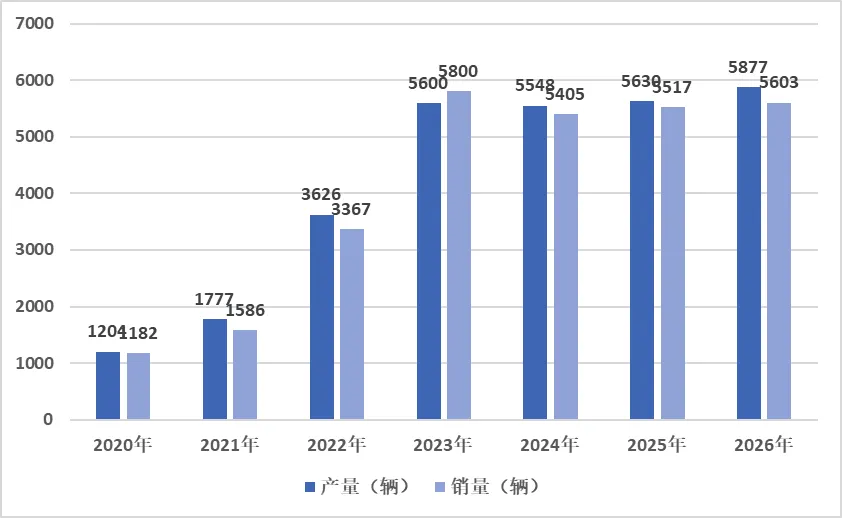

Public perception often associates hydrogen energy first with fuel cell vehicles, which have indeed entered a phase of rapid development. In August 2021 and January 2022, the “3+2” demonstration city clusters for fuel cell vehicles were approved, covering 47 cities across Beijing-Tianjin-Hebei, Shanghai, Guangdong, Henan, and Hebei. By March 2025, a total of 15,850 fuel cell vehicles had been deployed in the five clusters. In 2025, national output and sales of fuel cell vehicles were projected to reach 5,630 and 5,517 units respectively.

Nonetheless, from the real demand structure, industrial hydrogen use remains the largest source of demand. Steel, chemicals, and refining are major hydrogen consumers, historically relying on high-carbon gray hydrogen. Replacing gray hydrogen with green hydrogen in these scenarios would yield far greater emission reductions and demand scale than the transportation sector. The Rocky Mountain Institute predicts that industrial scenarios will remain the largest market for hydrogen demand by 2060.

In addition, the value of hydrogen energy as a long-duration energy storage and cross-regional regulation tool in the new power system is gradually emerging. As renewable energy penetration rises, demand for flexibility and peak-shaving capacity will grow. Hydrogen holds irreplaceable advantages in the “wind-solar–electricity–hydrogen–electricity” conversion chain. By the end of 2024, at least seven hydrogen-related distributed generation projects had been completed across Gansu, Yunnan, Guangdong, and other regions.

The 15th Five-Year Plan May Become a Critical Watershed for Hydrogen Energy

Since the release of the 15th Five-Year Plan recommendations in October 2025, national and local governments have continued to strengthen hydrogen policies. In November alone, 39 hydrogen-related policies were issued, including 10 national policies and 29 from 24 provinces and cities such as Beijing, Shanghai, and Jiangsu Dafeng, covering the entire chain including hydrogen refueling stations, direct green power connections, fuel cells, and hydrogen transportation.

Policy positioning for hydrogen during the 15th Five-Year Plan is undergoing a subtle but critical shift. If the 14th Five-Year Plan emphasized “demonstration” and “exploration,” the 15th Five-Year Plan places greater weight on systematic layout, business model exploration, and market mechanism development.

Recent policies reflect this direction:

The National Energy Administration proposed “scientific planning of infrastructure such as transmission pipelines, refueling and transfer ports, and orderly promoting cross-provincial transmission systems.”

Chengdu’s carbon peaking pilot plan aimed to “accelerate the construction of a half-hour hydrogen refueling network.”

Liaoning encouraged “exploring hydrogen-electricity coupling development models.”

Inner Mongolia required green power direct-connected hydrogen projects to fully participate in electricity market transactions.

In the next five years, policy focus will shift from subsidizing individual projects to guiding the industry toward self-sustainability through planning, standards, infrastructure, and financial instruments. Local governments and state-owned capital are transitioning from “subsidy promoters” to “industrial organizers” and “long-term capital providers.” Those that build a sustainable hydrogen industrial chain based on resource endowments, industrial foundations, and application scenarios will gain an edge in the next phase.

Hydrogen from an Investment Perspective: Structural Opportunities, Not Universal Ones

From an investment standpoint, hydrogen energy is not a sector suitable for full-scale expansion. It is a long-term industry that demands strategic patience, professional judgment, and scenario understanding.

Relatively high-certainty opportunities lie in:

Core equipment suppliers at the hydrogen production end, such as electrolyzers.

Core material suppliers for fuel cells, including proton exchange membranes, catalysts, and bipolar plates.

Solution providers deeply integrated with industrial hydrogen scenarios (green ammonia, green methanol), with strong technical reliability and long-term order potential.

Conversely, caution is needed for projects highly dependent on short-term subsidies, with unclear business models, and lacking technical or scenario barriers.

The development of hydrogen energy has never been a straight line. It is a long, sloped path requiring crossing multiple technical, cost, and institutional thresholds.

At this stage, hydrogen may still not be an immediate investment hotspot, but it is no longer just a conceptual future narrative. With clearer policies, a maturing industrial chain, and falling cost curves, hydrogen is steadily moving toward a more tangible and worthy long-term focus.

What truly matters is not “whether hydrogen will succeed,” but who can find a position aligned with the industry’s rhythm along the way.

Source: Chen Xun, Investment Department II

Reviewed by: Xue Yao

Released by: You Yi