If you have further insights or opinions on this article, please contact the author:Zhang Surong, General Manager of Investment Department IV, Nanjing Innovation Investment GroupEmail: zhangsr@njicg.com

Brief Analysis of Key Development Points in the Humanoid Robot Industry

01 Industry Development Context

Over the past three years, the humanoid robot sector has witnessed a new round of explosive growth, mainly driven by progress in Tesla’s robot projects and key industry events:

In May 2022, Elon Musk announced the launch of the first Tesla Bot prototype at AI Day on September 30, triggering the first market wave.

Between January and February 2023, the Ministry of Industry and Information Technology issued the "Robot +" Application Action Implementation Plan, and OpenAI released ChatGPT, which went viral online. The faster-than-expected development of large AI models further fueled the momentum.

From May to July 2023, Tesla unveiled the latest progress of Optimus, and Jensen Huang promoted the concept of "embodied intelligence", both drawing widespread attention, after which local governments successively introduced policies supporting humanoid robots.

Several recent landmark events completely ignited the overall market of the humanoid robot industry chain:

In May and October 2024, Shanghai and Beijing inaugurated the "National-Local Joint Humanoid Robot Innovation Center" and the "National-Local Joint Embodied Intelligence Humanoid Robot Innovation Center" respectively.

In January 2025, Unitree Robotics appeared on the CCTV Spring Festival Gala.

In April 2025, the Beijing Robot Marathon was held.

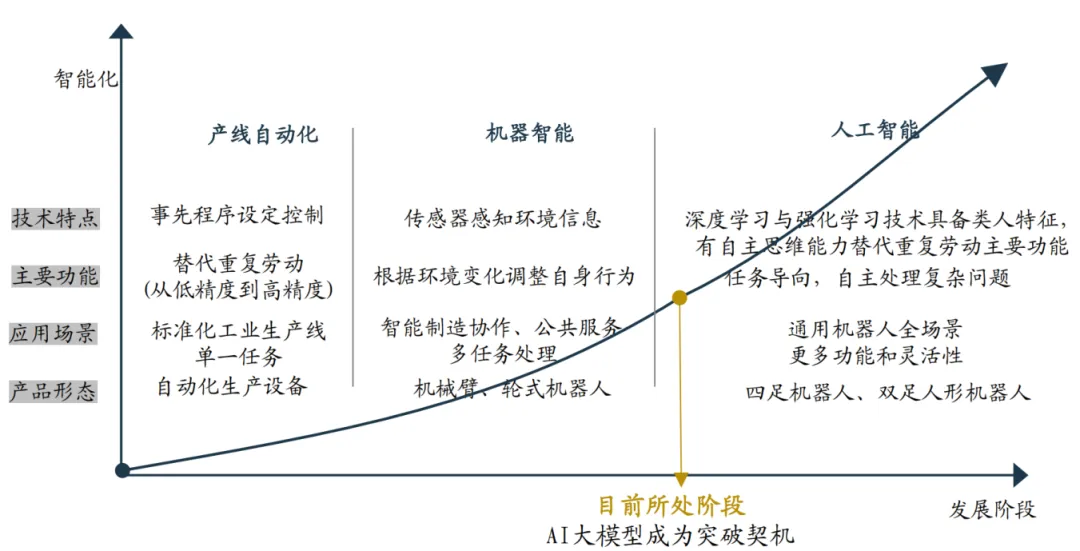

02 Industry Development Process

Embodied intelligence is one of the important paths to artificial general intelligence (AGI). Human intelligence largely depends on continuous interaction between the body and the environment. Embodied intelligence provides a similar growth environment for AI, enabling it to learn and evolve in the real world like humans.

When AI gains a physical body, its application scope expands from the digital world to the boundless physical world — from material handling on industrial production lines, elderly care in nursing institutions, to personalized services in future households. Embodied intelligence is empowering AI technology across all industries.

Technological advances are driving AI’s migration from digital space to physical space.

In terms of software development:Robot systems initially integrate perception-based information systems, then evolve into reasoning-oriented model systems, and finally achieve interaction with the environment and control over the physical world.

In terms of hardware development:The industry has evolved from early industrial robots based on motion rules, to collaborative robots with autonomous navigation and execution, and ultimately to embodied robots with one or more human-like functions.

Key technical challenges include extreme demand for computing power, acquisition of high-quality training data, and ethical issues such as ensuring safety and reliability in complex physical environments. These challenges are also driving forces for continuous technological breakthroughs.

03 Market Size

According to GGII (Gaogong Industry Research Institute):

In 2025, global sales of humanoid robots are expected to reach 12,000 units, with a market size of approximately 6.4 billion yuan.

By 2030, global sales will approach 340,000 units, with a market size exceeding 64 billion yuan.

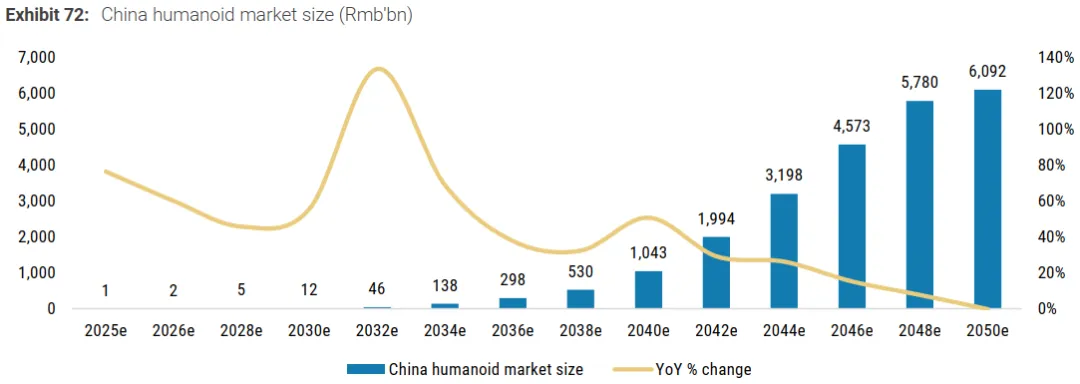

According to Morgan Stanley’s report Humanoid Robots 100: Mapping the Humanoid Robot Value Chain published in February 2025:

The total potential market size of humanoid robots could reach $60 trillion.

By 2050, China’s humanoid robot market is projected to reach 6 trillion yuan.

04 Industrial Chain

From the perspective of the robot itself

"Brain" (Decision-Making Intelligence)Refers mainly to large AI models, responsible for high-level cognitive tasks such as understanding language commands, recognizing objects in the environment, and planning task steps. Large models enable robots to become intelligent agents capable of understanding complex instructions and knowledge transfer, rather than tools limited to pre-set programs.

"Cerebellum" (Motion Control)Refers mainly to motion control algorithms, which translate decisions from the "brain" into smooth and precise physical movements, controlling coordination, balance, and posture. A strong "cerebellum" is critical for robots to run, jump, and perform delicate operations.

"Body" (Physical Platform)The carrier for interaction with the physical world, including sensors (cameras, tactile sensors) and actuators (joint motors). Its design directly affects perception and mobility, and is evolving toward greater flexibility and bionics to adapt to complex environments.

From the industrial chain perspective

Upstream: Core hardware and software (core control system, motion control system, motors, reducers, sensors, lead screws, etc.)

Midstream: Robot platforms / main bodies

Downstream: Industry applications (industrial, logistics, medical, household, etc.)

Current industry structure: downstream demand is still being cultivated; midstream competition is intense.

05 Constraining Factors

Despite high industry enthusiasm, humanoid robots still face difficulties in commercialization, mainly due to:

Technological breakthroughs: To achieve large-scale commercialization, humanoid robots must integrate mobility, interaction, and operation capabilities with high universality, generalization, and autonomous decision-making. Embodied intelligence is still in the early stage, resulting in insufficient application scenarios and relatively basic functions.

Product costs: Overall costs remain high, and core components urgently need cost reduction.

Fund Investment Strategy

01 Track Investment Status

Humanoid robot technology is accelerating from laboratory R&D and proof-of-concept to large-scale commercial application. The industry investment logic is shifting from early-stage "trend-chasing" and "concept consensus" to focusing on enterprises’ industrial implementation capabilities.

Companies with mass production, delivery, and commercialization capabilities are strongly favored by capital. At present, three core technical modules are the focus of investment and breakthroughs:

"Brain" (decision-making intelligence)

"Cerebellum" (motion control)

"Joints & Actuation" (precision execution)

Corporate tier differentiation is obvious:

Leading enterprises have completed multiple financing rounds with large single amounts, capturing most capital in the market.

Mid-tier and early-stage companies are mostly in technical verification and scenario exploration, with significant gaps in funding and valuation.

02 Investment Risk Factors

Technical maturity: Weak generalization of the "brain", insufficient stability of the "cerebellum", and unimproved precision and reliability of the physical body.

Cost & commercialization: High costs of core components, unaffordable prices for most scenarios, lack of scale effects, and high manufacturing costs.

Supply chain & standards: High-end components rely on customization; training data lacks unified standards; product quality is uneven; testing, certification, communication, and interfaces lack industry norms.

Ecosystem & scenarios: Downstream applications are fragmented; no consumer-facing "killer application" has emerged beyond B-end scenarios such as industrial handling and special operations.

Performance delivery: Some enterprises face overvaluation and bubbles. Capital markets now focus on order fulfillment and scalable profit closure rather than technical stories. High valuations will face severe tests if revenue and profit growth lag behind, leading to further corporate differentiation.

03 Investment Layout Strategy

Short-term: Focus on upstream componentsCore hardware, software, and component suppliers from manufacturing and automotive chains are relatively mature, providing short-term investment and layout opportunities.

Medium-term: Focus on midstream robot platformsCore competitiveness lies in breakthroughs in key technologies (especially motion control), scenario innovation, and financing capacity. We will focus on leading platform companies with potential for public markets, which can build moats through continuous capital support.

Long-term: Focus on the AI "Brain"Three mainstream technical routes currently exist:

End-to-end models represented by Tesla Optimus

"Fast-slow brain" hierarchical models represented by Figure AI

Brain-like partitioned architectures

None are yet optimal in model performance, computing efficiency, or sample efficiency, leaving large room for iteration. Companies developing robot "brains" and projects achieving large-scale commercial scenario implementation are strategically favored for the long term.

04 Investment Project Selection Criteria

Team background: Top interdisciplinary talent; strong financing and engineering capabilities; firm entrepreneurial determination. Priority to serial entrepreneurs, executives from well-known companies, and scientist-founders.

Technical strength: Clear and feasible technical routes; robust performance in real environments; potential to build long-term data and technical barriers.

Resources & supply chain: Control over core supply chains; cost advantages; cross-technology integration; internal resource synergy.

Commercialization strategy: Clear target markets and customer value propositions; viable business models (e.g., RaaS); clear paths for product definition and mass production delivery.

Source: Zhang Surong, General Manager of Investment Department IV

Reviewed by: Xue Yao

Released by: You Yi