I. Overview of Brake-by-Wire Chassis

Chart: Schematic Diagram of Brake-by-Wire Chassis

1. Core Definition and Technical Architecture

Perception Layer: Acquires road conditions and vehicle status through millimeter-wave radar, lidar, high-definition cameras, integrated inertial navigation, 4G/5G positioning, ADAS/high-precision maps, etc.

Decision Layer: The autonomous driving domain controller (ADC) and chassis domain controller (CDCU) complete perception fusion, navigation and positioning, decision planning and control command output.

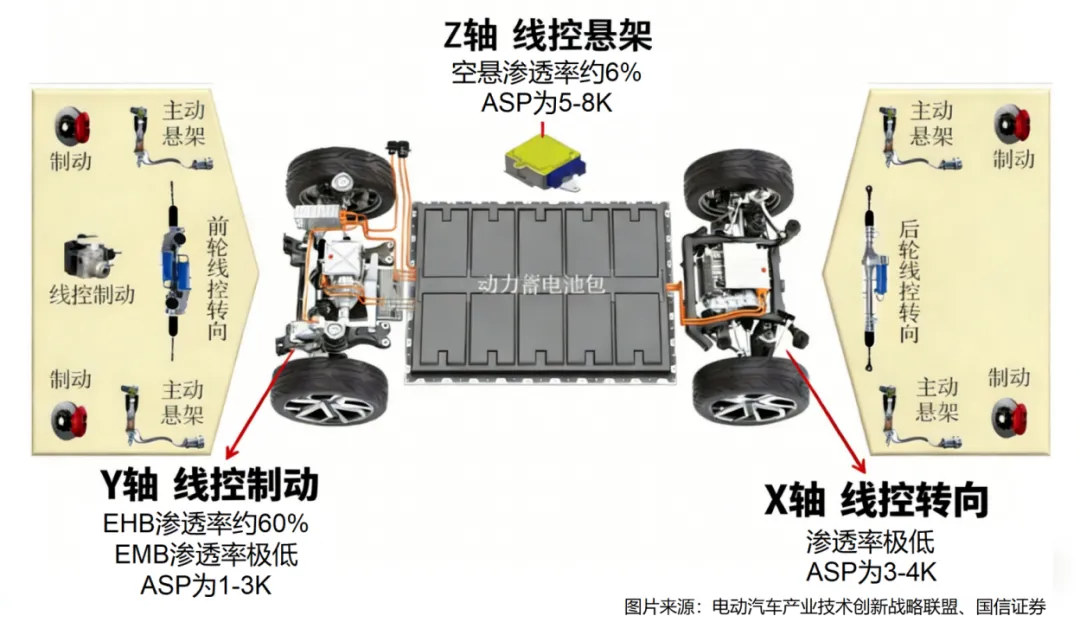

Execution Layer: Realizes dynamic control of the vehicle's XYZ three-direction and six-degree-of-freedom through five subsystems: steer-by-wire, brake-by-wire, active suspension, shift-by-wire and drive-by-wire.

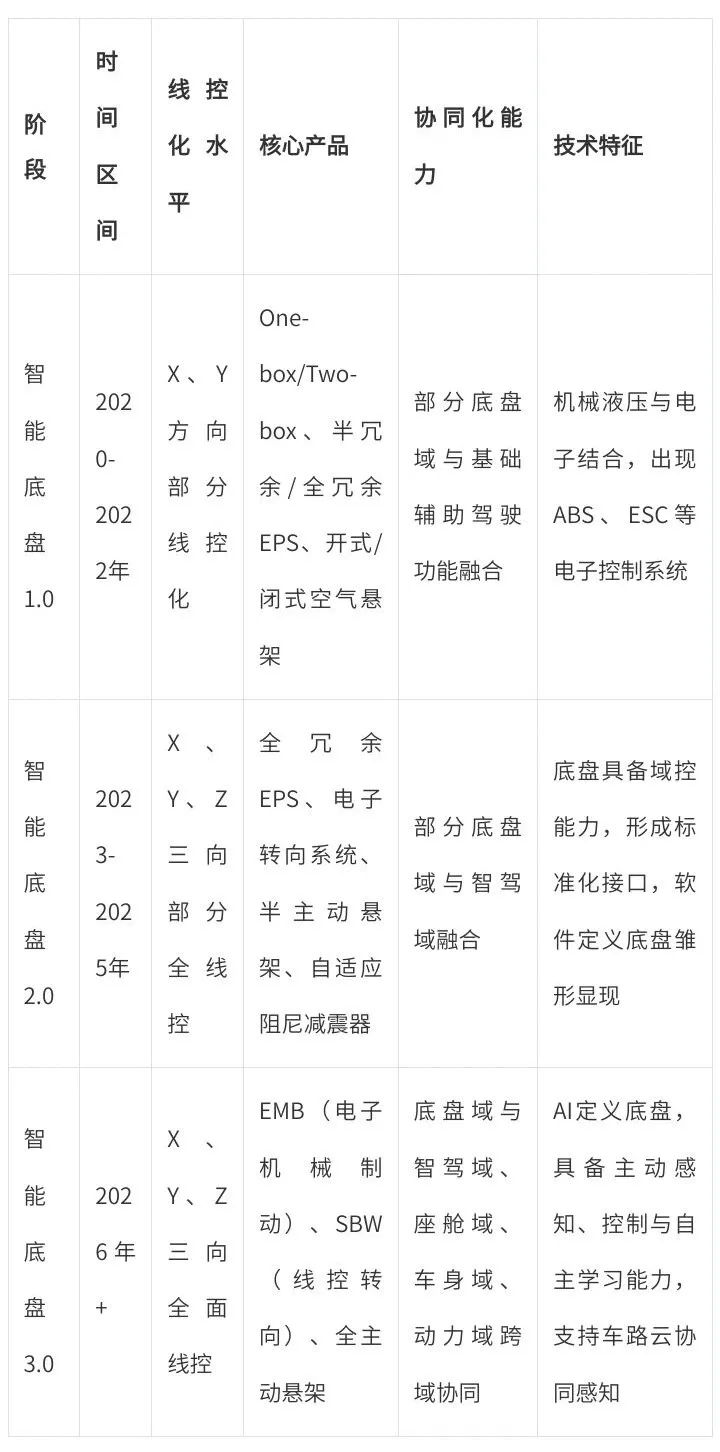

2. Development Stage: 2020-2030

3. Core Trends: Domain Control Integration and Cross-Domain Collaboration

Intra-domain Integration: By improving the integration of subsystems, it realizes coordinated control of XYZ three-direction and six-degree-of-freedom, optimizing the vehicle's dynamic performance such as lateral stability, vibration attenuation capability and steering flexibility.

Cross-domain Integration: Breaks the boundaries between the chassis domain and the autonomous driving domain, cockpit domain and body domain, and promotes the linkage of vehicle intelligent functions. For example, the in-depth coordination between the braking system and the AEB (Autonomous Emergency Braking) and ACC (Adaptive Cruise Control) functions of the autonomous driving domain.

Technology Evolution: Upgrades from "electromechanical hybrid" to "full drive-by-wire". Chassis control evolves from distributed ECU to chassis domain control and power-chassis fusion control, and finally moves towards central domain control integration, simplifying the electronic and electrical architecture, reducing wiring harness costs and improving data transmission efficiency.

4. Evolution Path of Domain Control Technology

II. Technology Iteration and Market Analysis of Brake-by-Wire

1. Core Definition and Core Value

The brake pedal position sensor captures the driver's intention and converts it into an electronic signal;

The electronic control unit (ECU) receives the signal and calculates the optimal braking force;

The drive actuator (hydraulic or electric motor) generates braking force, and feeds back the pedal feel through algorithms.

Adaptation to New Energy Vehicles: Gets rid of the dependence on vacuum source and solves the pain point of electric vehicles without engine vacuum assistance.

Support for Autonomous Driving: The response speed is increased by more than 30% compared with traditional braking, and some products are ≤90ms, meeting the precise control requirements of high-level autonomous driving for the execution end.

Energy Saving and High Efficiency: Decouples braking and energy recovery, which can increase the cruising range of electric vehicles by 5%-10%.

2. Technical Routes: EHB Leads the Present, EMB Leads the Future

(1) Electro-Hydraulic Brake (EHB): Current Mainstream of the Market (80% Market Share)

Retains hydraulic pipelines and integrates ABS/ESC units, divided into two schemes:

(2) Electro-Mechanical Brake (EMB)

Shorter response speed: 80ms vs 150ms of EHB, close to the limit of human nerve reflex;

More streamlined system: Eliminates hydraulic pipelines, brake fluid and booster, reducing vehicle assembly and maintenance costs by more than 30%;

Better performance: Zero drag (improves cruising range), lower noise (far from the cockpit) and lighter weight;

Higher integration: Can integrate parking (EPB) and driving braking functions, reducing assembly processes by 1-2 steps.

Safety Redundancy: Needs to meet ASIL-D level safety requirements, solve the problems of thermal management of wheel-side motors and high-temperature recession resistance of permanent magnets, and realize "dual-circuit redundancy";

Durability: Needs to pass 2.2 million fatigue durability tests with a service life of about 2300 hours;

Core Components: Wheel-side motors need to operate stably in extreme cold of -40℃ to high temperature of 120℃ and strong vibration environment. Gearboxes need to withstand greater torque, and ball screws need to be used instead of traditional thread transmission;

Cost Control: The current system cost is 1.4-3 times that of traditional hydraulic systems, and it is expected to be equal to the cost of hydraulic systems in 2026.

(3) Electronic Parking Brake (EPB): Pioneer Application of Drive-by-Wire Technology

Independent Type: Equipped with a separate EPB ECU with high cost;

Integrated Type: Integrates EPB and ESC into one controller, reducing ECU cost and wiring harness complexity. Enterprises need to have ESC production capacity or cooperate with ESC suppliers. Most domestic manufacturers rely on international ESC suppliers.

3. Industrial Chain Panorama: From Core Components to Terminal Applications

(1) Industrial Chain Structure

Upstream: EHB/EMB general components (solenoid valves, PCBs, automotive-grade MCU chips), brake motors (permanent magnet DC brushless motors, permanent magnet synchronous motors), sensors (pressure/temperature/wheel speed/steering angle sensors), brakes (caliper, brake disc);

Midstream: Brake-by-wire system integrators (foreign Tier 1, domestic listed companies, start-ups);

Downstream: Passenger vehicles, commercial vehicles, special vehicles, and automotive aftermarket.

(2) Upstream Core Links and Representative Enterprises

(3) Competition Pattern of Midstream System Integrators

EHB Market: Foreign leaders include Bosch (iBooster/IPB) and Continental (MKC1); domestic enterprises such as Bethel Automotive Safety Systems, Fudi Power, Liketech, and Nasen Technology have ranked among the top ten.

EMB Market: Overseas companies such as Brembo and Bosch plan mass production in 2025; domestic enterprises such as Bethel, Liketech, Tongyu Electronics, Coordinate System, Gelubo, and Jingxi are accelerating their layout.

4. Market Scale: Hundred-Billion-Yuan Track Expands Rapidly

(1) EHB Market

Penetration Rate: In 2024, the assembly volume of brake-by-wire EHB exceeded 10 million units, a substantial year-on-year increase of 61.4%. From January to July 2025, the assembly volume of EHB was close to 6 million units, and it is expected that the annual assembly volume of EHB will exceed 12 million units in 2025. In terms of assembly rate, the annual assembly rate is expected to exceed 50% in 2025.

Market Size: Expected to exceed 20 billion yuan in 2025.

(2) EPB Market

In 2022, the front-loading standard configuration of domestic passenger vehicles was 16.7358 million units, with a penetration rate of over 80%;

The market size was 12 billion yuan in 2023 (passenger vehicles accounted for 85%), and it is expected to reach 18.3 billion yuan in 2025 with a penetration rate of 90%;

Competition Pattern: Bosch, Huayu Automotive Systems, Continental Group, Ningbo Huaxiang Electronics, etc.

(3) EMB Market (Mass Production First Year in 2026)

Key Assumptions: Annual passenger vehicle sales increase by 2%; brake-by-wire penetration rate is 60% in 2025/70% in 2030; EMB proportion is 1% in 2025/40% in 2030; EMB ASP is 2500 yuan in 2025/1681 yuan in 2030;

Market Size: Installation volume will increase from 140,000 sets in 2025 to 7.13 million sets in 2030, with a scale exceeding 10 billion yuan;

Penetration Rate: The penetration rate of new energy vehicles will exceed 15% in 2028, and the penetration rate of L3+ models will exceed 50% in 2030.

III. Investment Logic: Driving Factors and Core Opportunities

1. Core Driving Factors

(1) New Energy Vehicles Replace Fuel Vehicles, Spurring Upgrading of Braking Systems

(2) Stringent Requirements of High-Level Autonomous Driving for the Execution End

(3) Policy and Regulatory Endorsement, Removing Obstacles for EMB Mass Production

(4) Rising Demand for Energy Recovery, Highlighting the Advantages of Brake-by-Wire

2. Core Investment Opportunities

(1) Accelerated Domestic Substitution, Continuous Increase in Market Share of Domestic Suppliers

(2) Technology Iteration Dividend: One-Box Leads the Present, EMB Layouts for the Future

One-Box: The penetration rate increased from 20.5% in 2021 to 65.1% in H1 2024, becoming the mainstream solution in the drive-by-wire market. Domestic enterprises such as Bethel, Liketech and Nasen Technology have achieved mass production;

EMB: The mass production first year in 2026 is approaching. Domestic enterprises have seized the technological high ground, which will trigger industry reshuffle in the next 3-5 years.

(3) Automakers' "Independent R&D + Co-R&D" Layout, Reconstructing the Supply Chain Ecosystem

(4) Segmented Track Opportunities: Domestic Substitution of Upstream Core Components

Automotive-Grade MCU Chips: Domestic enterprises such as CoreWise Microelectronics, CoreTitan Technology and Xpeedic Technology have achieved breakthroughs in ASIL-B/D level products, with substitution space exceeding 10 billion yuan;

Sensors: Foreign capital accounts for more than 70% of pressure sensors, IMU and other products. Enterprises such as Amperor Electronics and Navitas Semiconductor are accelerating import substitution;

Brake Calipers: The high-end market is monopolized by Brembo and Continental. Domestic enterprises such as Bethel and Yatai Co., Ltd. are accelerating their layout, with domestic substitution space exceeding 5 billion yuan.

Source: Guo Shaobin, Investment Department II

Reviewer: Xue Yao

Publisher: You Yi