Key Points in the Process of Non-Public Agreement Transfer of State-Owned Equity in Listed Companies

For further insights and thoughts on this article, please contact the authors:Han Jiakang & Tang Yu, Compliance Management Department, Nanjing Innovation Investment GroupE-mails: hanjk@njicg.com, tangy@njicg.com

Against the backdrop of the deepening reform of state-owned enterprises and the increasing frequency of capital market operations, the non-public agreement transfer of state-owned equity in listed companies has become an important way for many enterprises to optimize their equity structure and promote resource integration. Different from public market transactions, such transfers have the dual attributes of safeguarding the security of state-owned assets and complying with the regulatory requirements of the securities market. They not only need to strictly prevent the loss of state-owned assets, but also meet the securities regulatory requirements such as information disclosure and equity registration.

Based on the regulatory system and practical experience summarized in a project of non-public agreement transfer of state-owned equity in a listed company, this paper systematically sorts out the core points of the transaction process, and intends to introduce them from the perspectives of the regulatory system, core transaction elements and subsequent compliance management, so as to provide actionable operational guidelines for relevant entities.

I. Regulatory Legal System Under the Dual Background of Listed Companies and State-Owned Equity

The non-public agreement transfer of state-owned equity in listed companies is essentially a combination of "state-owned asset transactions" and "securities market activities", and thus must comply with two types of rules simultaneously. Before advancing the transaction, it is first necessary to straighten out the regulatory legal system of the two types of rules and clarify the compliance boundaries of the transaction.

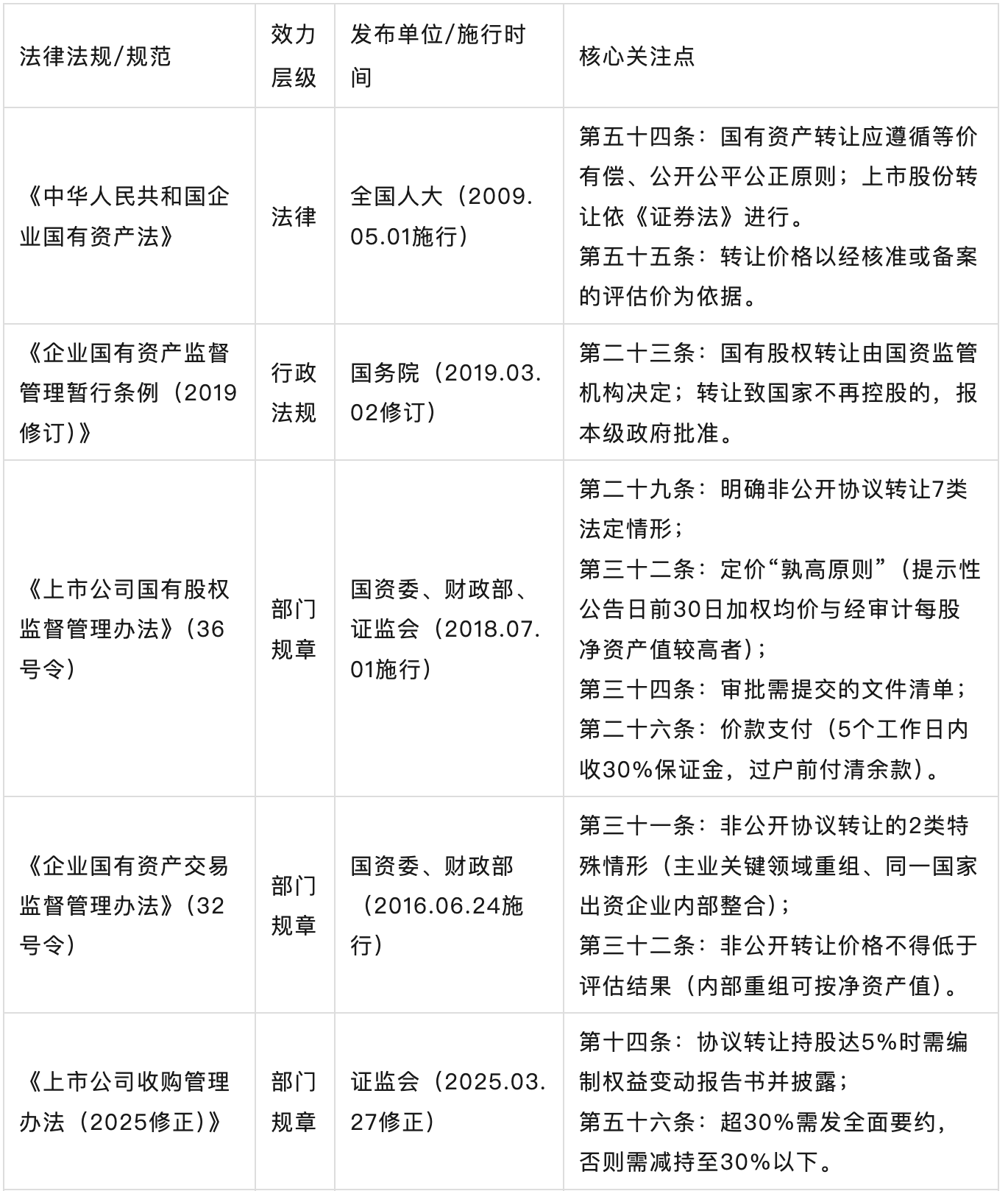

(I) Core Legal and Regulatory System

It can be seen from the above system that Decree No.36, Decree No.32 and the Measures for the Administration of Takeovers of Listed Companies are the most frequently cited core documents in practice. All aspects of the transaction, including preconditions, pricing and procedures, must be based on these rules as the fundamental basis.

(II) Logical Application in Areas with Unclear Rule Connection

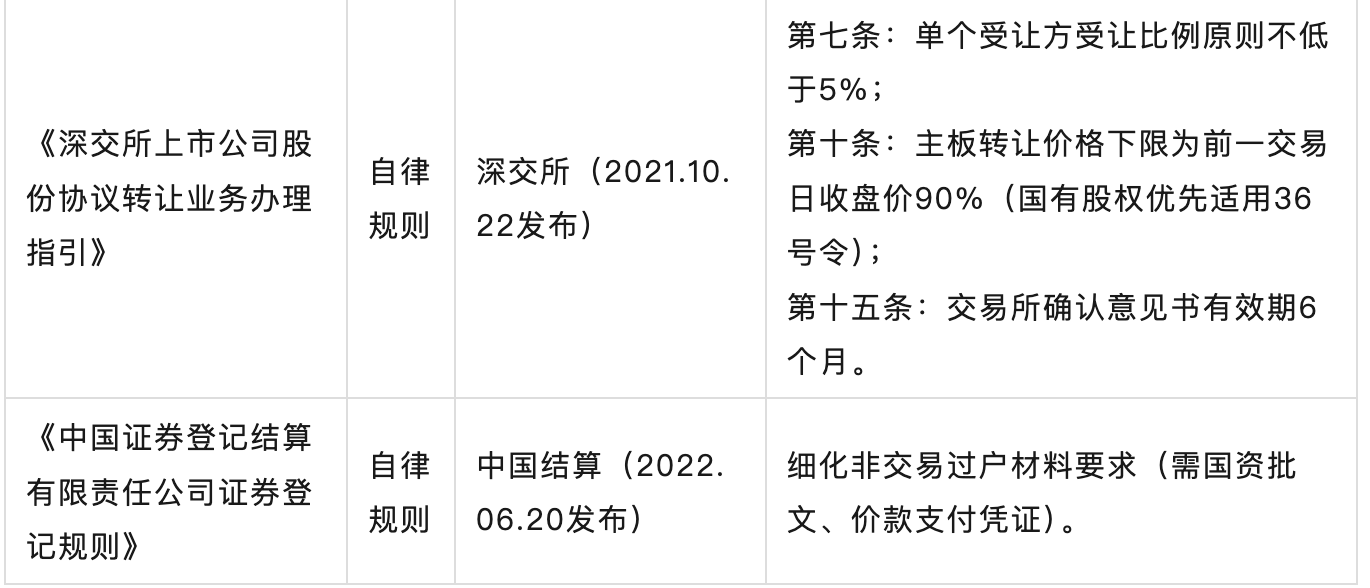

Based on the combing of the regulatory rule system, it can be found that although the two types of rules complement each other in the two major fields of state-owned asset supervision and capital market supervision, there are also areas with unclear connection at the provision level. A common conflict in practice is reflected in the differences of the "pricing rules" in the two rule systems.

Article 3.5.4 of the Shenzhen Stock Exchange Trading Rules stipulates that the declared price of an agreement block transaction of a security with a price limit shall be determined within the price limit range of the security on the current trading day. Article 3.3.13 of the Trading Rules stipulates that the price limit ratio for main board stocks is 10%. That is, the transfer price of main board stocks shall not be lower than 90% of the closing price of the previous trading day. However, Decree No.36 clearly stipulates that the pricing of state-owned equity shall take the higher of the 30-day weighted average price and the audited net asset per share. There are differences in the pricing rule standards between the two. Article 10 of the Guidelines for the Handling of Agreement Transfer of Shares of Listed Companies on the Shenzhen Stock Exchange stipulates: "The agreement transfer of shares of a listed company shall take the closing price of the transferred shares in the secondary market on the trading day prior to the date of signing the agreement as the pricing benchmark, and the lower limit of the transfer price range shall be implemented in accordance with the provisions on block transactions, unless otherwise stipulated by laws, administrative regulations, departmental rules, normative documents and the business rules of this Exchange". Based on this, the authors believe that for the relevant rules involving the pricing of state-owned equity transfer, if there are special provisions by the state-owned asset supervision department, such provisions shall prevail. Decree No.36 and the exchange guidelines should be in the nature of a special provision and a general provision respectively. Accordingly, the state-owned equity transfer shall apply Decree No.36 as a special provision in priority, and is not subject to the 90% restrictive provision of the exchange.

II. Core Elements of Non-Public Agreement Transfer of State-Owned Equity in Listed Companies

After clarifying the aforementioned legal and regulatory framework for such transactions and combining with the actual difficulties in practice, the authors believe that the key elements for the implementation of the transaction can be summarized into six links: applicable scenarios, pricing, procedures, approval, disclosure and registration. These links need to ensure compliance in combination with the specific circumstances of the transaction.

(I) Applicable Scenarios for Non-Public Agreement Transfer

According to Article 29 of Decree No.36, the non-public agreement transfer method can only be adopted if the following 5 statutory scenarios are met, which also serve as the preconditions for the non-public transaction of state-owned equity in listed companies:

A listed company has suffered losses for two consecutive years and is at risk of delisting, and the transferee has put forward a clear restructuring plan;

The core business of a listed company belongs to the key areas related to national security and the lifeline of the national economy, with special qualification requirements for the transferee;

In the integration of state-owned resources or asset restructuring, both the transferor and the transferee are state-owned shareholders;

A listed company repurchases its shares or makes a tender offer, or a state-owned shareholder transfers its shares due to dissolution, bankruptcy, capital reduction and other reasons;

A state-owned shareholder contributes with its held shares of a listed company (e.g., capital injection into other state-owned enterprises).

(II) Pricing Method: The "Higher of the Two" Principle as the Bottom Line, and Approval Required for Special Cases

Since the pricing of state-owned equity transfer is directly related to the security of state-owned assets, the State-owned Assets Supervision and Administration Commission (SASAC) will also focus on such matters when reviewing relevant transaction documents. Based on the aforementioned explanation of the connection between Decree No.36 and the exchange rules, the pricing rules shall apply the relevant provisions of Decree No.36.

Basic Pricing Applies the "Higher of the Two" PrincipleThat is, the higher of the "arithmetic average of the weighted average prices for the 30 trading days prior to the date of the prompt announcement" and the "audited net asset per share in the most recent fiscal year" shall be taken as the transfer base price, and the pricing shall not be lower than this standard.

Pricing Flexibility in Exceptional CircumstancesThe negotiated pricing by the transferor and the transferee considering factors such as net asset per share, return on net assets and price-earnings ratio is only allowed in the circumstance of "integration/restructuring of state-owned resources without reduction of state-owned equity interests". Even so, such pricing must be approved and confirmed by the state-owned asset supervision authority.

The two parties to the transaction shall first reach a preliminary intention on the negotiated pricing plan, engage professional institutions (such as securities firms and asset appraisal institutions) to demonstrate the rationality of the pricing plan, and submit the pricing plan, demonstration report and other relevant materials to the state-owned asset supervision authority for approval. Such approval is subject to certain uncertainties; if the approval is not obtained, the pricing plan shall be readjusted.

(III) Transfer Procedures

From internal decision-making to the final transfer of ownership, the entire equity transfer process has strict requirements and strong timeliness due to the involvement of state-owned assets and the equity of listed companies. Before the transaction is carried out, the rights and obligations of all parties and the time schedule for the decision-making process should be designed in advance to avoid the impact of procedural matters on the progress of the transaction. The following supplements the specific operational steps, required materials, time cycle and precautions for each procedural link:

Internal Decision-Making: The transferor and the transferee shall each perform the relevant decision-making procedures in accordance with the requirements of their respective company articles of association and internal systems and form written resolutions (the shareholder representatives of state-controlled enterprises shall vote in accordance with the instructions of the state-owned asset supervision authority and issue a written report);

State-Owned Asset Approval: If the transfer is not conducted within the same group, it shall be reported to the state-owned asset supervision authority for approval. The provincial-level state-owned asset supervision authority may delegate the approval authority to the municipal level under certain circumstances (see II/(IV) List of Documents for SASAC Approval in this section for details);

Signing of Agreement: Clarify the number of target shares, pricing basis and payment method (it is required to stipulate that "a 30% deposit shall be paid within 5 working days, and the balance shall be paid in full before the transfer of ownership");

Information Disclosure: If the shareholding ratio of the transferee reaches 5%, the transferee shall prepare a Equity Change Report (abbreviated or detailed) within 3 days from the date when the shareholding ratio reaches 5%. The Equity Change Report shall include the basic information of the transferee, the number and proportion of the transferred shares, the transaction price and pricing basis, source of funds, purpose of the transfer, shareholding plan within the next 12 months, associated relations with other shareholders of the listed company and other contents. The transferee shall submit the Equity Change Report to the China Securities Regulatory Commission (CSRC) and the stock exchange, and disclose it by issuing an announcement through the listed company;

Stock Exchange Review: The transferor and the transferee shall jointly submit the Application Form for Confirmation of Share Transfer, the state-owned asset approval document, the payment voucher and other materials to the stock exchange, which shall complete the completeness check within 3 trading days;

Transfer Registration: After the transferee pays the full consideration, the transferor and the transferee shall jointly apply to China Securities Depository and Clearing Corporation (CSDC) for equity transfer registration with the Letter of Confirmation of Share Transfer (valid for 6 months) issued by the stock exchange and the full consideration payment voucher.

(IV) List of Documents for SASAC Approval

According to Article 34 of Decree No.36, a complete list of materials shall be submitted when applying to the state-owned asset supervision authority for approval to avoid delays in approval due to incomplete materials. The specific material requirements are as follows:

Internal decision-making documents of the transferor and the transferee;

Equity transfer plan (with a detailed explanation of the pricing basis and transaction purpose);

Feasibility study report;

Equity transfer agreement;

Legal opinion issued by a law firm;

Due diligence report issued by a financial advisor (if the transfer of controlling rights is involved);

The most recent fiscal year's financial reports of the transferor and the transferee.

(V) Core Requirements for Stock Exchange Information Disclosure

Securities market supervision has strict requirements for the timeliness, accuracy and completeness of information disclosure. In practice, it is necessary to plan the work schedule and plan in advance around the 5% shareholding ratio threshold.

Initial Disclosure: When the transferee's shareholding reaches 5% for the first time, the Equity Change Report shall be disclosed within 3 working days and announced through the listed company;

Subsequent Disclosure: The Equity Change Report shall be disclosed repeatedly for every 5% increase or decrease in the shareholding ratio (e.g., from 5% to 10%, or from 10% to 5%);

The disclosure content shall include the transaction price, number of shares, pricing basis, background of the transferee (e.g., actual controller, core business) and other information, with no key information omitted.

(VI) Registration and Settlement

CSDC has clear requirements for the transfer of ownership: the Letter of Confirmation of Share Transfer issued by the stock exchange, the state-owned asset approval document, and the full consideration payment voucher (delivery voucher for non-monetary assets) must be submitted, and the requirement that "the full consideration has been paid before the transfer of ownership or has been entrusted to a third party" must be met; otherwise, the transfer registration will not be processed.

III. Post-Transfer Compliance Management

The completion of equity transfer registration does not mean the full conclusion of the transaction. The transferee still needs to continuously pay attention to the relevant restrictions on subsequent information disclosure and share reduction to avoid regulatory penalties due to compliance omissions.

1. Subsequent Information Disclosure

Disclosure of Equity Change Information: Within 2 days after the completion of the transfer of ownership, the listed company shall disclose an announcement on the results of the equity change, clarifying the final shareholding ratio, date of completion of the transfer of ownership and the transferee's subsequent shareholding plan.

Disclosure of Major Matters: If the transferee becomes a shareholder holding more than 5% of the shares, any subsequent major matters with the listed company that may affect the stock price, such as asset replacement and connected transactions, shall be disclosed in a timely manner in accordance with the Measures for the Administration of Information Disclosure of Listed Companies (2025 Revision), without delay or concealment.

2. Restrictions on Share Reduction

In accordance with the Securities Law and the Several Provisions on the Reduction of Shares by Shareholders, Directors, Supervisors and Senior Managers of Listed Companies, the transferee must comply with the relevant provisions when reducing its shares.

Prohibition of Short-Term Trading: No sale of shares within 6 months after purchase, or no purchase within 6 months after sale; the proceeds from such transactions shall belong to the listed company. At present, the regulatory authorities adhere to the "one-end principle" in the actual review process, that is, short-term trading is constituted as long as the transferee has the status of a shareholder holding more than 5% of the shares at either the "purchase or sale" stage.

Restrictions on the Proportion of Share Reduction:

Call Auction Trading: The number of shares reduced shall not exceed 1% of the total share capital of the listed company within any consecutive 90 natural days;

Block Trading: The number of shares reduced shall not exceed 2% of the total share capital of the listed company within any consecutive 90 natural days;

Agreement Transfer: The transferee and the transferor shall share the 1% call auction share reduction quota within 6 months (i.e., the total number of shares reduced by both parties shall not exceed 1%).

IV. Practical Details

Combined with project experience, the following three details, although not clearly emphasized in the core regulations, also constitute the key points for the implementation of the transaction and should therefore be paid attention to.

1. Mandatory Requirements for State-Owned Asset Appraisal

In accordance with the Measures for the Administration of State-Owned Asset Appraisal (2020 Revision), asset appraisal must be conducted for the agreement transfer of state-owned equity, and the appraisal results must be approved or filed by the state-owned asset supervision authority (Article 32 of Decree No.32). Direct transfer without appraisal is strictly prohibited to prevent the loss of state-owned assets.

2. Tax Treatment

Transferor (state-owned shareholder): Subject to enterprise income tax (transfer income × 25%), value-added tax (6% tax rate in accordance with "financial commodity transfer") and stamp duty (transaction amount × 0.05%);

Transferee: Subject to stamp duty on paid-in capital (paid-in capital contribution × 0.025%).

It is recommended to jointly calculate the tax burden with the financial and tax teams at the initial stage of the transaction to avoid the impact of tax issues on the transaction progress in the later stage.

3. Transitional Period Arrangements: Clear Stipulation of Voting Rights and Profit/Loss Bearings

There is usually a transitional period of 1 to 3 months from the signing of the agreement to the transfer of equity ownership. It is recommended to clarify the following contents in the Equity Transfer Agreement:

Ownership of voting rights of the target shares during the transitional period: Since the share transfer has not been completed, the voting rights shall in principle still be exercised by the transferor, but it may be stipulated that major matters such as asset restructuring and external guarantees require the written consent of the transferee.

Bearing of profits and losses of the target shares during the transitional period: In principle, the income generated by the target shares during the transitional period (such as dividends) shall still belong to the transferor, and similarly, the losses shall be borne by the transferor. However, it is recommended to clearly define the benchmark date for profit and loss calculation, which is usually the date of signing the agreement.

Response to stock price fluctuations: If there is a large fluctuation in the stock price, for example, the stock price fluctuates by more than 5% during the transitional period or the period exceeds 3 months, it may be stipulated that a re-appraisal is required and the number of shares is adjusted accordingly.

Conclusion

As an important carrier for the optimal allocation of state-owned capital and the resource integration of listed companies, the entire process of the non-public agreement transfer of state-owned equity in listed companies must strictly connect the dual rules of state-owned asset supervision and the securities market, and has the dual attributes of compliance and practicality. From the determination of applicable scenarios before the start of the transaction, to the implementation of the "higher of the two" principle in the pricing link, the control of the completeness of materials in the approval process, and then to the information disclosure and share reduction compliance management after the transfer of ownership, each link must be based on laws and regulations and focus on risk prevention and control. On the premise of ensuring the security of state-owned assets, we should improve transaction efficiency and the effect of resource integration, and help state-owned capital achieve high-quality operation in the capital market.

Source: Han Jiakang, Tang Yu, Compliance Management Department

Reviewer: Xue Yao

Publisher: You Yi