In June 2023, Apple officially launched its first MR device, the Vision Pro, which features Micro OLED screens for its internal displays, making it the first product to incorporate Micro OLED technology. According to relevant parties' cost breakdown of the Vision Pro, the two Micro OLED screens account for nearly 50% of the total device cost. Following Apple's adoption of Micro OLED display technology, several major manufacturers have followed suit. For instance, devices such as the AIR 3 released by Thunderbird and the high-end headset Aoxue Vision Max launched by Aoxue Technology have also adopted this technology. Currently, Micro OLED is gradually becoming the mainstream technology in the XR microdisplay market.

Micro OLED, also known as OLEDoS (OLED on Silicon), is a novel display technology that integrates semiconductor manufacturing processes with OLED technology, utilizing monocrystalline silicon wafers as the substrate to produce OLED devices. The industry chain can be referenced in the figure below, specifically including upstream raw materials, silicon-based backplanes, assembly components, manufacturing and testing equipment; midstream Micro OLED panel manufacturers; and downstream various terminal applications.

In the critical midstream display manufacturing segment of Micro OLED, Japanese and South Korean companies currently hold the major market share. Among them, Japan's Sony dominates the global Micro OLED panel market and is also a core supplier for the Vision Pro. Against the backdrop of domestic panel manufacturers intensifying efforts to expand production capacity, how to conduct legal due diligence for such panel factory projects has become the main issue explored in this article.

Focus on the construction status of the company's existing production capacity.

01 Construction progress of the company's existing production lines

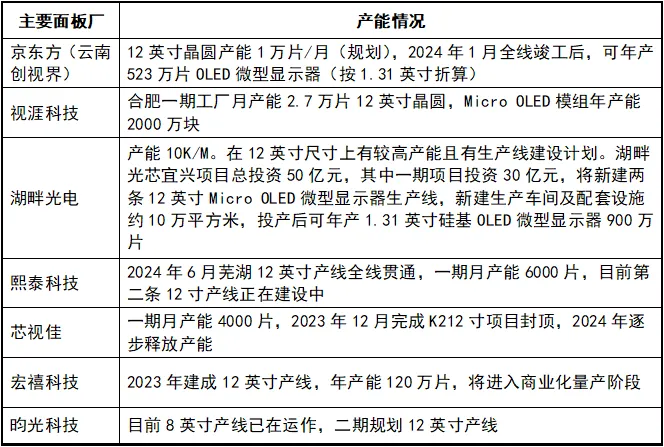

According to incomplete statistics, the current construction status of domestic Micro OLED production lines is as follows:

Data source: Official websites and public accounts of various companies.

According to the above statistics, due to the ongoing cost reduction demands in downstream consumer electronics, domestic manufacturers have gradually begun constructing 12-inch production lines. If the project company has not yet considered this layout or is still in the process of building a 12-inch line, it will be at a disadvantage compared to competitors in terms of both production capacity assurance and cost reduction space when dealing with customers. Therefore, it is necessary to verify on-site which of the following stages the company's 12-inch production line construction has reached: ① equipment evaluation stage; ② equipment move-in stage; ③ equipment installation and debugging stage; ④ process debugging stage; ⑤ product (note: "product" is typically translated as "product" in this context, as it refers to a specific technical step in display or semiconductor manufacturing where the product is first powered and tested. If you meant a different interpretation, please provide more context).

02 Funding composition of production line construction

According to industry standards in the micro-display sector, establishing a complete Micro OLED 12-inch production line requires equipment investment exceeding RMB 1 billion, with factory construction and land development costing several hundred million RMB, bringing the total fixed asset investment to over RMB 1 billion. It is crucial to verify the certainty of funding sources for the production line construction, including equity financing, debt financing progress, and the company’s self-raised capital, to avoid delays due to unmet fundraising expectations. Additionally, attention must be paid to the mortgage status of the company’s key production equipment. Given that display manufacturing is a capital-intensive industry, continuous external financing is essential. During debt financing, banks often require mortgaging critical production equipment. Therefore, it is necessary to assess the company’s short- and long-term financial liabilities, potential off-balance-sheet debts, and the risk of key equipment being seized due to failure to repay loans.

03 Procurement status of core equipment

Currently, core equipment for 12-inch production lines still relies on imports, including evaporation systems, lithography machines, development and etching equipment, and thin-film deposition devices. Among these, evaporation systems alone cost over RMB 200 million per unit, representing the largest single investment in equipment. Major suppliers of evaporation systems are primarily Japanese and Korean manufacturers, such as Japan’s Canon Tokki and Korea’s Sunic System. Although these devices are not currently subject to export restrictions, potential impacts from geopolitical tensions or trade conflicts could hinder the import of advanced evaporation systems, significantly jeopardizing the project company’s production line development.

Due diligence on equipment procurement must verify whether the company’s primary suppliers are mainstream manufacturers and review the status of signed procurement contracts. It is critical to confirm whether delivery timelines are explicitly stipulated in these contracts to avoid delays in production line commissioning caused by late equipment arrivals.

Focus on the expansion of downstream major customers

Review all signed sales contracts to analyze existing customers: conduct interviews to understand specific application scenarios and determine whether shipped products are integrated into their core offerings; use third-party data to estimate total shipment volume of devices incorporating the company's products, given primary downstream applications such as XR devices; analyze the number of major customers over the years to assess repurchase rates and new client acquisition, thereby evaluating customer recognition of the company's products. If the customer base is unstable, further investigate whether product stability or quality issues exist.

Based on industry expert interviews, aside from SeeYA Technology and BOE, other panel manufacturers in China have not yet achieved mass production of 12-inch Micro OLED products. It is essential to verify the company's progress in engaging with potential clients—whether it is at the RFI stage for technical specifications or the RFQ stage for specific project inquiries. Due diligence should include reviewing email correspondence and meeting minutes with major clients, as well as conducting interviews to confirm whether factory audits have been completed and if the company has been approved as a qualified supplier by potential customers.

Focus on the company's core technical capabilities

The Micro OLED production process comprises four core stages: drive IC design, anode fabrication, evaporation, and thin-film encapsulation. Due diligence on panel manufacturers should involve verifying the quality and quantity of the company’s patent portfolio in key process segments, as well as yield data across stages, to comprehensively assess whether the project company possesses core technologies.

01 Drive IC design capability

Verify whether the company independently owns chip design capabilities by reviewing outsourced R&D contracts and patents in chip design. If feasible, conduct interviews with wafer suppliers. If the company claims independent drive backplane design capabilities, validate the technology source by examining the resumes and prior experience of chip R&D personnel to confirm mastery of display drive IC design.

Given that Japanese and Korean manufacturers hold numerous drive circuit patents, request a detailed comparison between the company’s design patents and existing patents from these manufacturers to assess potential infringement risks.

02 Anode fabrication and evaporation process

This stage is critical for enhancing product brightness and yield. Verify evaporation equipment procurement contracts and require performance metric test reports for each process segment to evaluate technical execution.

03 Thin-film encapsulation process

This stage determines product lifespan and reliability, with atomic layer deposition being a key equipment. Verify the company’s encapsulation process patents and request reliability test reports to assess core technical capabilities in thin-film encapsulation.

Domestic Micro OLED production is currently transitioning from “technological breakthrough” to “mass production.” Therefore, when investing in panel manufacturers, prioritize companies with:Existing 12-inch production lines and sufficient construction funding;Strong downstream key account partnerships (e.g., deep ties with major manufacturers);Independent core technical capabilities (e.g., proprietary intellectual property).

Beyond project-specific risks, even if the company possesses core technologies and mature mass-produced products, ultimate investment decisions must hinge on evaluating the actual controller. Understanding the actual controller is fundamental to project investment.

Source: Compliance Management Department, Zhang Zheng

Cover image source: Xinhua News Agency

Reviewed by: Xue Yao

Published by: You Yi