If you have further insights or ideas about the article, please contact the author: Liu Jing, Risk Control Department, Nanjing Innovation Investment Group, liuj@njicg.com

01 Introduction

The core of financial due diligence (FDD) in traditional industries lies in predicting future operating conditions by reviewing historical operational data. However, for the emerging commercial space sector, characterized by high capital intensity, technology-driven nature, high risks, high barriers to entry, and disconnect between valuation and financial statements, non-financial factors exert a significant decisive influence on financial outcomes. Therefore, FDD for such enterprises is usually not limited to financial statements themselves; its core lies in penetrating financial figures to conduct dual verification of "technical feasibility" and "commercial economy". Currently, the emerging commercial space sector encompasses various business forms such as rocket manufacturing and launch services, satellite platform and payload manufacturing, and satellite communication operation and services, covering the entire industrial chain from manufacturing and launch to operation and application. This article mainly focuses on discussing financial due diligence strategies in the current emerging commercial space sector.

02 Typical Risks

We have sorted out the typical risks that the emerging commercial space sector may face, as follows:

(1) Revenue Sustainability Risk

Emerging commercial space companies exhibit distinct characteristics in operating income: revenue lags significantly behind R&D investment, revenue scale is highly dependent on the industrial ecosystem, and revenue sustainability faces substantial uncertainty.

(2) Risk of Failure to Meet Cost Reduction Expectations

The traditional aerospace model is "ensuring success regardless of cost", while the logic of emerging commercial space is "achieving the unity of reliability and economy through innovation and high efficiency". Currently, most companies in the emerging commercial space sector are in the R&D or small-batch production stage. Meanwhile, suppliers of numerous key components, special materials, and test benches in this sector are still units within the "national team" system or enterprises restructured from them, and some supply chains are replaced by domestic channels, leading to the risk that future cost reduction may not meet expectations.

(3) Technical Uncertainty Risk

R&D in the emerging commercial space sector is often characterized by high capital investment, multi-disciplinary technical collaboration, long R&D cycles, and high trial-and-error costs. At present, the overall technical path has been clarified, but large-scale and high-reliability engineering applications are not yet mature, resulting in significant technical uncertainty risks.

(4) Capital Chain Break Risk

The emerging commercial space sector is a typical capital-intensive industry. Before generating stable cash flow, companies remain in a long-term cash-burning state of "only inflows without outflows" and are highly dependent on external cash flow. Capital chain break constitutes a major "sudden death" risk for such enterprises.

(5) Core Team Stability Risk

In a highly uncertain environment, "people" are the only core variable capable of responding to changes and creating certainty. Investment is essentially investing in people, so the stability of the core team is crucial for the long-term operation of the company.

(6) Risk of IPO Process Disruption and Narrowed Investor Exit Channels

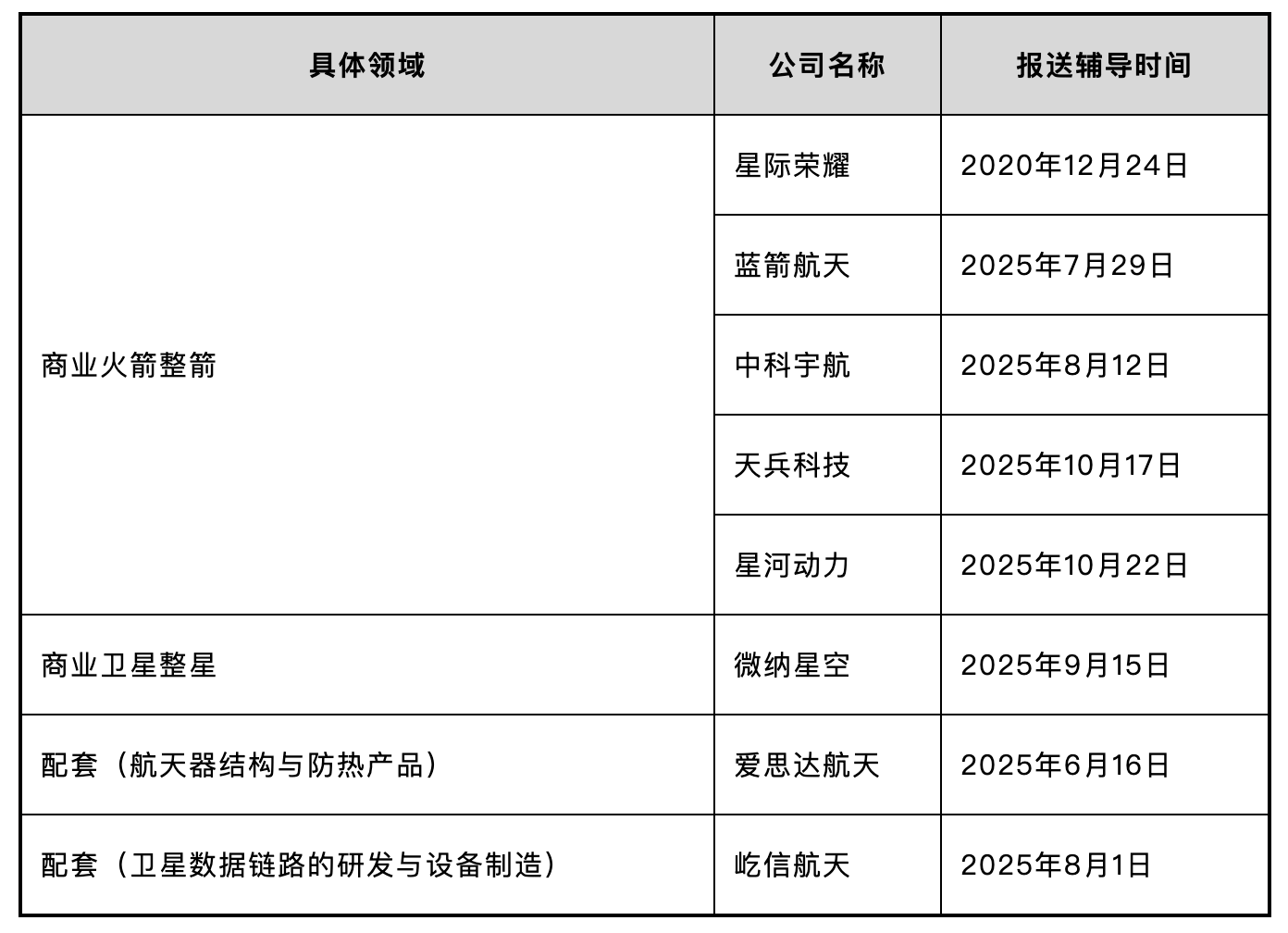

In June 2025, the China Securities Regulatory Commission (CSRC) restarted the listing rules for unprofitable enterprises applying the fifth set of standards on the Science and Technology Innovation Board (STAR Market). This standard downplays short-term profitability and focuses more on core technologies, market potential, and long-term value, which is highly consistent with the characteristics of emerging commercial space companies. As of mid-to-late October 2025, a total of 8 commercial space companies have conducted IPO counseling registration, with specific details as follows:

Source: Compiled based on public information.

Except for iSpace, which initiated counseling earlier, other companies basically started listing counseling after the policy was issued. Currently, emerging commercial space companies have an unprecedented enthusiasm to enter the capital market. However, if the company's IPO process is disrupted due to unclosed internal technical or commercial paths, or changes in external regulatory policies, the investment return cycle will be significantly prolonged, and exit channels will face the risk of narrowing.

03 Due Diligence Strategies

In response to the above typical risks, we have summarized the typical financial due diligence strategies from previous projects:

(1) Prudently Verify Operating Income and Demonstrate Revenue Sustainability

1. Verify the Authenticity and Reasonableness of Revenue Recognition

Obtain transaction-related documents such as contracts, acceptance documents, invoices, and bank statements for walk-through tests, and conduct comparative analysis with the payment terms, delivery and acceptance standards, and breach and return clauses stipulated in sales contracts. Interview core customers and confirm transaction details. Verify the subsequent collection and return of accounts receivable from major customers, and analyze the matching between revenue growth and sales collection.

2. Analyze Current Revenue Drivers and Clarify the Revenue Contribution of Core Products

Before the large-scale commercialization of core products, early-stage commercial space companies often carry out transitional businesses to maintain operations. For example, rocket engine R&D companies may temporarily provide test bench testing services, customized software development services, or even trading services to customers to obtain short-term cash flow. Therefore, during due diligence, it is necessary to clarify the contribution of core product revenue to the company's total revenue and analyze the support of large-scale technical service contracts (of entrusted R&D nature) for revenue sustainability. Analyze the correlation between different types of businesses and demonstrate their mutual synergy and driving effects.

3. Pay Attention to Customer Concentration and Background

Currently, the main customers of commercial space companies include institutional units and leading commercial space enterprises, making them prone to relying on a small number of "national team" and giant customers. Therefore, it is necessary to monitor changes in the demand of core customers. For major customers, especially those established recently but having generated significant transactions and those with mismatched backgrounds and transaction volumes, conduct in-depth verification through public channels, peripheral interviews, and other methods.

4. Monitor Constellation Networking Dynamics and Analyze the Expected Conversion of Existing Orders

Based on the company's product characteristics, confirm the target constellation types (such as high-low orbit constellations, communication/navigation/remote sensing constellations). Classify existing orders provided by the company by product type, customer segment, and order form (common forms include white lists, letter of intent framework contracts, pre-production agreements, and formal sales orders). Exclude "existing orders" often used to inflate numbers, such as letter of intent framework contracts and white lists. Analyze the execution progress of each order in combination with constellation construction schedules and historical production and delivery cycles to estimate the approximate timing of revenue recognition for existing orders. For example, when conducting due diligence on enterprises providing inter-satellite laser communication equipment for satellite networks, pay attention to the connection between existing orders and the launch time/batch/quantity of satellite networks to fully match downstream demand.

(2) Focus on Production Model Scalability and Supply Chain Diversification to Evaluate Future Cost Reduction Potential

1. Evaluate the Scalability of Existing Production Models and Monitor Industrial Chain Closure

Understand the existing production model. For example, for rocket/engine R&D companies, check whether they have self-built or long-term locked final assembly workshops. If outsourcing final assembly, verify the independent control of key processes (such as tank welding and engine assembly), and whether they have exclusive engine test benches, launch pads, or long-term rental contracts (including emergency backups) to avoid production scheduling uncertainty caused by "waiting for national team slots". Meanwhile, conduct comparative analysis in combination with material procurement, equipment investment, and personnel division of labor to assess whether the current small-batch production model can support future large-scale growth.

2. Analyze the Company's Cost Structure

Analyze the composition of operating costs by direct materials, direct labor, and manufacturing overhead, and cross-verify with the production model. Obtain detailed cost breakdowns of individual products and compare them with data from comparable industry peers to confirm the company's cost competitiveness. For example, when conducting due diligence on satellite platform propulsion systems, compare the cost of a single propulsion system with that of institutional units and private enterprises. Obtain and analyze the company's underlying BOM (Bill of Materials) structure. For instance, rocket engines can be further disassembled into subsystems such as combustion devices, turbo pumps, valves, final assembly, and electrical systems. Understand the current status of BOM for each subsystem and the company's specific future cost reduction measures, such as relying on economies of scale, optimizing design, improving automation, and domestic substitution of core components, to comprehensively judge the feasibility of cost reduction.

3. Pay Attention to Supply Chain Concentration

Sort out the supplier layout of core materials and demonstrate the rationality of high supply chain concentration in combination with industrial chain conditions. Monitor the company's supplier development efforts and analyze the stability of the supply chain and the potential for improving bargaining power in the future.

(3) Reasonably Evaluate R&D Investment and Verify R&D Progress Through Multiple Channels

1. Verify the Accuracy of R&D Expense Recognition

Disaggregate R&D expenses by expense nature, focus on the specific composition of R&D expenses, and prioritize verifying large-scale outsourced R&D and cooperative R&D to assess the company's dependence on external core technologies. Obtain and verify R&D personnel rosters, working hour records, and payrolls to ensure that labor costs are correctly allocated to corresponding R&D projects and prevent production or management personnel costs from being included in R&D expenses. Track large-scale R&D material requisitions to confirm their use in specific R&D projects.

2. Focus on R&D Investment Directions

Interview the company's core technical team to understand the reasons for technical route selection and compare its advantages and disadvantages with mainstream solutions [e.g., for rocket engine R&D enterprises, focus on technical routes of solid engines, liquid oxygen kerosene engines, and liquid oxygen methane engines; for satellite propulsion system R&D enterprises, focus on differences between chemical propulsion systems and electric propulsion systems (krypton and xenon propellants)]. Obtain the list of R&D projects for historical periods and the next 3 years, focus on core R&D links, and compare them with the company's publicly stated technical routes.

3. Verify R&D Progress as Stipulated in Milestone Agreements

Based on the R&D milestone plans provided by the company (e.g., detailed plans for engine R&D enterprises include key nodes such as overall scheme design, subsystem design, subsystem ignition tests, and full-system tests), compare planned and actual completion status and analyze the specific reasons for project delays. Request the company to provide key evidence of milestone achievements, such as third-party testing reports/test reports/expert review reports, test data (including important technical indicators such as duration, thrust, and specific impulse), and on-orbit operation data.

4. Pay Attention to the Formation of Intellectual Property Rights

Typically, large-scale R&D investment should result in high-quality intellectual property rights with protective barriers. Therefore, through the intellectual property list provided by the company, evaluate the correlation and matching with core R&D projects, and pay attention to the acquisition methods of intellectual property rights.

(4) Reasonably Estimate Future Capital Needs Based on Historical Capital Usage

1. Analyze Historical Capital Usage

Request the company to provide detailed historical bank statements and verify whether the use of large funds is abnormal. Obtain the usage of previous financings, compare them with the original business plans based on historical cash flow statements, and sort out the historical path of the company's capital allocation. Analyze core turnover indicators and solvency indicators to monitor the company's capital safety margin.

2. Reasonably Estimate Future Capital Needs

Based on current cash reserves and operational capacity indicators, calculate the duration the company's existing funds can support operations. Clarify the specific use of the current round of financing, such as R&D, production expansion, or covering operating losses. Formulate detailed and feasible capital expenditure plans according to R&D milestone plans and match investment amounts accordingly.

(5) Evaluate the Stability of the Core Team

1. Focus on Core Team Background and Organizational Integrity

Core teams of commercial space companies mostly come from the "national team". Therefore, by sorting out resumes, pay attention to their complete career trajectories and demonstrate the support of their institutional project experience for current entrepreneurship. Cross-verify the educational background, work experience, and project experience of core personnel through public website information and external resources. Obtain the company's organizational structure chart to determine whether the established team can systematically cover the core links from technical realization to commercial success.

2. Focus on Remuneration and Equity Incentives of Core Personnel

Obtain payrolls, focus on the composition of the company's remuneration system, and analyze the linkage between performance bonuses and quantifiable technical milestones. Demonstrate the matching degree between core personnel's remuneration and their positions, and conduct comparative analysis with the remuneration of personnel in the same functions of comparable industry peers. Obtain the company's equity incentive plan, confirm the scope of authorization and exercise period, and calculate the impact of share-based payments on the company's profits. Obtain the list of employee departures and monitor changes in core personnel.

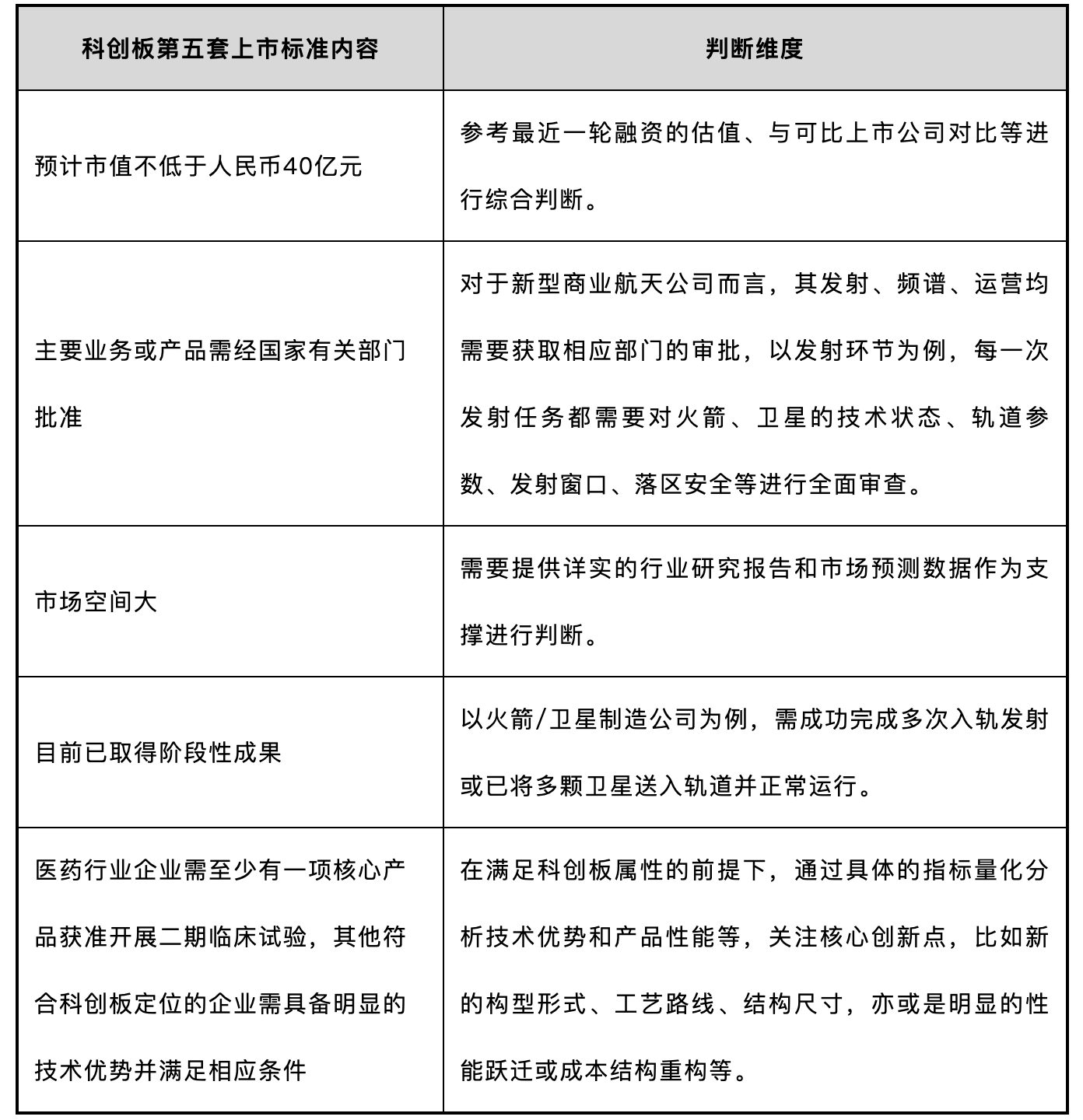

(6) Match Investment Terms According to Investment Strategies and Objectives

Combined with the fifth set of listing standards on the STAR Market, industrial laws, and experience from previous projects, the company's IPO progress can be judged from the following dimensions:

Source: Compiled based on public information.

The fifth set of standards on the STAR Market is by no means a "get-out-of-jail-free card for losses". Even if the company fully meets the rigid indicators such as market value and technology, it may still fail in the rigorous review and inquiry process. Therefore, for companies in the emerging commercial space sector, we suggest paying more prudent attention to the repurchase entity, repurchase liability, and repurchase period to maximize the protection of their own interests.

04 Summary

Most emerging commercial space companies are currently in the early stages with high potential risks. When conducting financial due diligence on such companies, it is possible to cross-verify specific situations such as revenue, costs, and R&D from multiple perspectives, while continuously tracking capital market dynamics and focusing on the review priorities of regulatory authorities. In addition, financial due diligence needs to closely cooperate with business due diligence and legal due diligence to draw a complete three-dimensional portrait of the target company.

Source: Liu Jing, Risk Control Department

Reviewer: Xue Yao

Publisher: You Yi