A Brief Discussion on the IPO Review Standards and Concepts for Projects with Related Party Transactions Accounting for More Than 30% of Total Transactions

With the vigorous implementation of the registration-based system centered on information disclosure, a number of enterprises with "related party transactions in specific industries accounting for 30% or even more of total transactions" have successfully passed the review. However, can the "30% threshold" for related party transactions be completely ignored or set aside? This article summarizes the latest IPO review standards and concepts by analyzing approved cases.

Main Board Provisions:

"Article 25 The issuer shall fully disclose related party relationships and appropriately disclose related party transactions in accordance with the materiality principle. The pricing of related party transactions shall be fair, and there shall be no manipulation of profits through related party transactions."

STAR Market & ChiNext Board Provisions:

"Article 12 The issuer shall have a complete business and the ability to operate independently and continuously in the market directly:

It shall have complete assets and independent operations, personnel, finance, and institutions. There shall be no horizontal competition with the controlling shareholder, actual controller, or other enterprises controlled by them that has a material adverse impact on the issuer, nor any related party transactions that seriously affect independence or are obviously unfair.

The issuer’s main business, control rights, management team, and core technical personnel shall be stable. There shall be no material adverse changes in the main business, directors, senior managers, or core technical personnel within the latest 2 years; the ownership of shares held by the controlling shareholder and shareholders dominated by the controlling shareholder or actual controller shall be clear, and there shall be no change in the actual controller within the latest 2 years, nor any major ownership disputes that may lead to changes in control rights.

The issuer shall have no major ownership disputes over main assets, core technologies, trademarks, etc., no major debt repayment risks, no major guarantees, lawsuits, arbitrations, or other contingent liabilities, and no material adverse changes in the business environment that would have a significant adverse impact on its continuous operation."

The following provisions are from Answers to Several Questions on Initial Public Offering Business (revised in June 2020):

Question 16: Issuers for initial public offerings (IPOs) generally have a certain proportion of related party transactions during the reporting period. As a potential listed company, from which aspects should the issuer explain the situation of related party transactions, and how to improve the information disclosure of related party transactions? What aspects should intermediaries pay attention to during verification?

Answer: During due diligence, intermediaries shall respect the issuer’s legitimate, reasonable, normal, and necessary business activities. If there are related party transactions, they shall conduct verification based on the principle of prudence regarding matters such as the legality, necessity, rationality, and fairness of the transactions, the identification of related parties, and the procedures for performing related party transactions. At the same time, the issuer shall provide sufficient information disclosure, specifically as follows:

dentification of related parties: The issuer shall identify and disclose related parties in accordance with the Company Law, Accounting Standards for Business Enterprises, and relevant regulations of the China Securities Regulatory Commission (CSRC).

Necessity, rationality, and fairness of related party transactions: The issuer shall disclose the content, amount, background of related party transactions, and the relationship between such transactions and the issuer’s main business; it shall also explain and summarize the disclosure of the fairness of related party transactions by referring to fair market prices, third-party market prices, prices between related parties and other counterparties, etc., and clarify whether there is any transfer of benefits to or from the issuer or related parties.

If the proportion of revenue, costs, expenses, or total profits corresponding to related party transactions between the controlling shareholder/actual controller and the issuer in the issuer’s corresponding indicators is relatively high (e.g., reaching 30%), the issuer shall fully explain and summarize the disclosure of whether the related party transactions affect the issuer’s operational independence, whether they constitute dependence on the controlling shareholder or actual controller, and whether there are situations such as adjusting the issuer’s revenue, profits, costs, or expenses through related party transactions or transferring benefits to the issuer. In addition, the issuer shall also disclose specific measures to reduce related party transactions with the controlling shareholder or actual controller in the future.

Decision-making procedures for related party transactions: The issuer shall disclose the provisions of its articles of association on the decision-making procedures for related party transactions, whether the decision-making process of existing related party transactions is consistent with the articles of association, whether related shareholders or directors have abstained from voting when deliberating on relevant transactions, and whether independent directors and members of the supervisory board have expressed different opinions.

Verification of related parties and related party transactions: Sponsors and the issuer’s lawyers shall conduct sufficient verification and issue opinions on the identification of the issuer’s related parties, the completeness of information disclosure on the issuer’s related party transactions, the necessity, rationality, and fairness of related party transactions, whether related party transactions affect the issuer’s independence or may have a material adverse impact on the issuer, and whether the decision-making procedures for related party transactions have been performed.

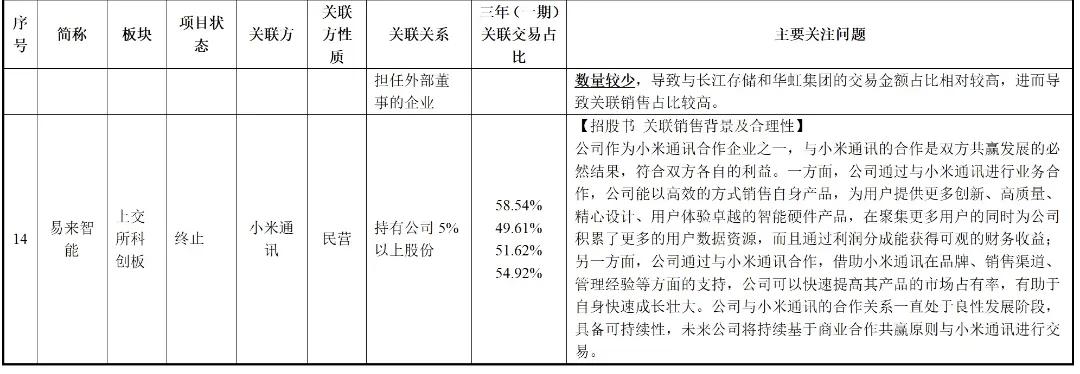

Up to now, the regulatory authorities have not set clear restrictions on the proportion of related party transactions of potential listed companies on the ChiNext Board and STAR Market during the reporting period. Case analysis shows that currently, there are relatively few cases on the ChiNext Board where the proportion of related party transactions during the reporting period is relatively high (exceeding 50%) and the company has been approved, and most of these cases are due to the particularity of the issuer’s industry. Therefore, to determine whether an excessively high proportion of related party transactions will affect a company’s listing, the following aspects shall be the key focuses:

The necessity and rationality of the existence of related party transactions;

The amount of related party transactions and their proportion in similar transactions;

Whether there is any "disguised non-related party transactions" (i.e., treating related party transactions as non-related);

Whether the internal control system for related party transactions is sound and effectively implemented;

Whether related party transactions have a material impact on the company’s business independence;

Whether the related party transactions have gone through necessary and standardized decision-making procedures and pricing mechanisms, and whether the issuer has formulated and implemented effective measures to reduce related party transactions;

The fairness of related party transactions, whether there is material dependence on related parties, and whether future related party transactions are sustainable.

From the above case sharing, it can be seen that the regulatory review attitude still adheres to the spirit of laws and regulations while respecting objective business rules. In addition to traditional industries with high downstream customer concentration (such as electric power, railways, and telecommunications), successful cases have also emerged in semiconductors and packaging materials. On the basis of sufficient information disclosure, an excessively high proportion of related party transactions is no longer a "one-vote veto" obstacle. Therefore, the following conclusions can be drawn:

Potential listed companies shall not have related party transactions that seriously affect independence or are obviously unfair. Independence and fairness are reflected in the fact that procurement or sales transaction decisions are based on the issuer’s own business demands and interests, rather than one-sided benefit transfer or input to cooperate with related parties. The analysis can be conducted from perspectives such as the upstream and downstream competitive pattern of the industry, the irreplaceability of technology, and the necessity, rationality, and fairness of transactions.

Although the proportion of related party transactions has occasionally exceeded the threshold recently, such cases are mainly concentrated in specific industries such as electric power, railways, and telecommunications. Considering that a large amount of third-party transaction data is required to prove qualitative indicators such as independence, fairness, and industrial status, it is recommended that for potential listed companies with private ownership, the proportion of related party transactions should be controlled below 50% as a threshold or target.

On the premise of complying with the objective laws of the industry, potential listed companies shall also take feasible measures to gradually reduce the proportion of related party transactions as much as possible, and plan in advance specific measures to reduce related party transactions with related parties in the future. After all, investors in the secondary market will also worry that the issuer may adjust its revenue, profits, costs, or expenses through related party transactions after listing, thereby affecting the valuation of the secondary market and the return rate of PE equity investment.

In summary, during the equity investment analysis process, for projects involving an excessively high proportion of related party transactions, higher requirements are imposed on the research of details such as industry structure, value chain analysis, competitive advantages, business models, financial due diligence, and governance structure. More prudence shall also be exercised when making investment decisions.