Zhang Surong

General Manager of the 4th Investment Department, Nanjing Innovation Investment Group

Education Background: Master of Software Engineering, Department of Computer Science and Technology, Nanjing University; Doctor of Management Science and Engineering, School of Economics and Management, Southeast University.

Work Experience: Previously worked at Nokia Siemens (Beijing), Huawei Technologies Co., Ltd., and Aerospace Zijing Investment Management Co., Ltd.

Professional Expertise: Possesses a compound professional background, with rich experience in investment research & analysis and equity investment in the pan-IT industry, including software information technology, artificial intelligence, and industrial internet.

Key Investment Projects Led: Ruikeda (688800), Kejia Co., Ltd. (STAR Market application submitted), Les Information (STAR Market application submitted), Speed China (ChiNext application to be submitted), etc.

Table of Contents

Overview of the Information Innovation Industry

1.1 Definition of the Information Innovation Industry

1.2 Industry Development History and Current Status

1.3 Policy Environment for Industry Development

1.4 Factors Affecting Industry Development

1.5 Industry Barriers

Market Scale and Industry Prospects

2.1 Market Scale

2.2 Development Prospects

Industrial Chain and Value Chain

3.1 Industrial Chain

3.1.1 Upstream - Underlying Hardware and Infrastructure

3.1.2 Midstream - Basic Software and Platforms

3.1.3 Downstream - Enterprise Applications and Solutions

3.1.4 Cross-Industry Chain - Information Security

3.2 Value Chain

3.3 Cost Structure

Investment Analysis

Analysis of Investment Opportunities in Core Segments of the Information Innovation Industry

5.1 CPU

5.1.1 Major Industry Participants

5.1.2 Target Company - Tianjin Phytium

5.2 Operating Systems

5.2.1 Major Industry Participants

5.2.2 Target Company - Kylin Software

5.2.3 Target Company - UnionTech Software

5.3 Storage

5.3.1 Major Industry Participants

5.3.2 Target Company - CXMT (Changxin Memory Technologies)

5.3.3 Target Company - YMTC (Yangtze Memory Technologies)

Conclusion

Chapter 1 Overview of the Information Innovation Industry

1.1 Definition of the Information Innovation Industry

Infrastructure (chips, storage devices, complete machines - servers/PCs, firmware, etc.);

Basic software (operating systems, middleware, databases);

Application software;

Information security.

1.2 Industry Development History and Current Status

Due to the leading position of the United States and other countries in science and technology in the past, China’s IT industry ecosystem was basically built on hardware and software from overseas technology enterprises, including:

CPUs (Intel, AMD, etc.);

Operating systems (Microsoft, Apple, etc.);

Databases (Oracle, Microsoft, etc.);

Middleware (IBM, Oracle, etc.);

Application software (Office, Adobe, etc.);

Security software (Kaspersky, ESET, etc.).

"2" refers to the Party and government institutions;

"8" refers to eight key industries: finance, telecommunications, petroleum, electric power, transportation, aerospace, hospitals, and education.

Table 1. Development History of China’s Xinchuang Industry

1.3 Policy Environment for Industry Development

Underlying hardware (servers, complete machines, chips) receives the strongest policy support;

Followed by enterprise applications (office software, industrial software, application software);

Then infrastructure (5G base stations, data storage centers, supercomputing centers).

1.4 Factors Affecting Industry Development

Unbreakthrough Key Technologies: Especially upstream core technologies, some of which are still monopolized by foreign enterprises, requiring further strengthening of technological research and resource support.

Product Shortcomings: Domestic products still face issues such as narrow application scope, poor compatibility, weak scalability, insufficient performance, poor versatility, and immature technology.

Limited Global User Base: The absolute number of users of the Xinchuang Industry globally is still difficult to compete with foreign giants. It is necessary to strengthen product R&D and marketing to gain user and market recognition internationally.

Fragmented Industry Pattern: There are few domestic leading enterprises with strong strength, and the industrial chain is relatively scattered. Facing international giants, it is still unable to leverage the advantages of synergy.

1.5 Industry Barriers

(1) Technical Barriers

(2) Qualification Barriers

Enterprises need to be included in the "Catalogue of Special Information Equipment" of the National Security Bureau;

The Ministry of Industry and Information Technology (MIIT) has also released a "Catalogue of Xinchuang Products", imposing high requirements on industries and enterprises;

To provide products and services to the military, enterprises need to obtain Level 2 or above military confidentiality qualification;

For system integration in party, government, military, and key industries, enterprises need to have confidential information system integration qualifications and operation and maintenance qualifications.

(3) Market Barriers

Party and Government Institutions: The overall replacement work is guided and promoted by the General Office of the Central Committee. The party committees’ general offices of provinces, cities, and ministries are responsible for leading the implementation. Models such as integrated projects, centralized procurement, and agreement-based supply coexist. Ministries and provincial authorities have strong discretion in technical routes, so it is necessary to adopt a "province-specific strategy" to target key directions for market development.

Key Industries: Customers in key industries include telecommunications, radio and television, finance, energy, transportation, water conservancy, emergency management, health care, social security, national defense science and technology industry, etc. The replacement work in these industries is mainly promoted by the science and information technology, and confidentiality departments of each industry, and organized and implemented by industry users. It requires system integration manufacturers with in-depth industry understanding.

(4) Talent Barriers

Chapter 2 Market Scale and Industry Prospects

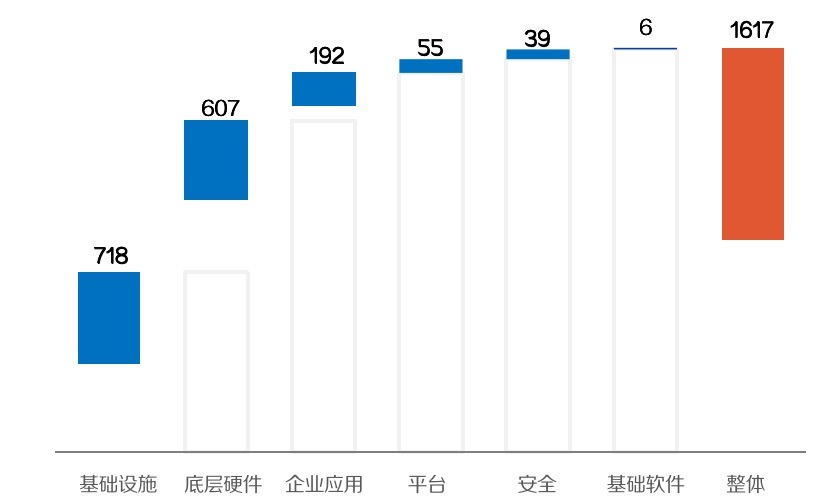

2.1 Market Scale

Infrastructure accounted for the largest share at 71.8 billion yuan;

Followed by underlying hardware at 60.7 billion yuan;

Enterprise applications at 19.2 billion yuan;

The market scale of platforms, security, and basic software was still relatively small.

Data Source: Haibi Research Institute

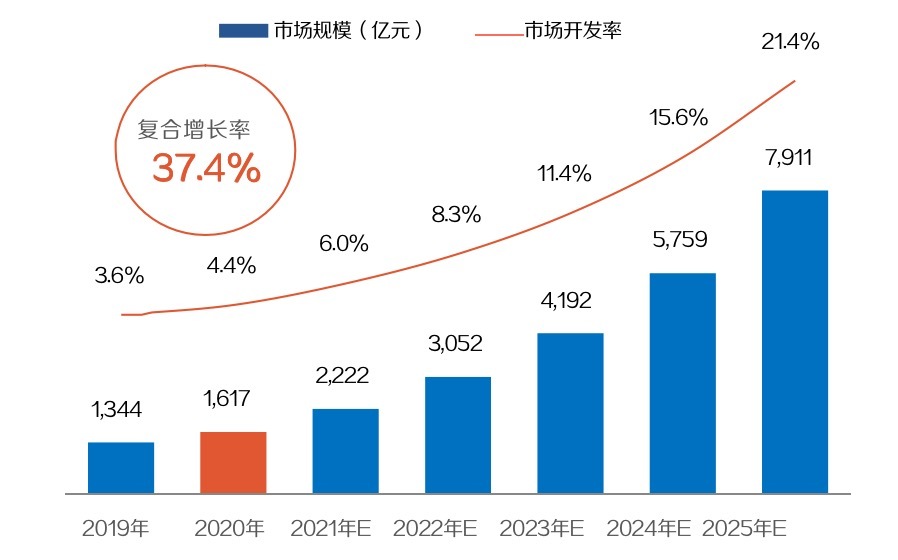

2.2 Development Prospects

The output value of the digital economy will account for 62% of the global GDP;

It will account for 67% of China’s GDP, exceeding the global average.

Data Source: Haibi Research Institute

According to IDC's forecast, by 2023, the global computer industry market will reach 1.14 trillion US dollars, and the investment space of China's computer industry will be 104.3 billion US dollars. Among them, the market space of China's server industry is about 238 billion yuan, the public cloud market is about 185 billion yuan, the enterprise application software market is about 99.8 billion yuan, the storage market is about 38 billion yuan, the basic software market is about 19 billion yuan, the big data platform software market is about 17.3 billion yuan, and the middleware market is about 9 billion yuan. From the data forecast, China's server, public cloud, enterprise application software and storage markets have huge development potential.

Figure 3. 2023 Forecast of Market Size for China's and Global Computer Industry (in 100 Million US Dollars)

Data Source: IDC, Zhongcheng Think Tank

Chapter 3 Industrial Chain and Value Chain

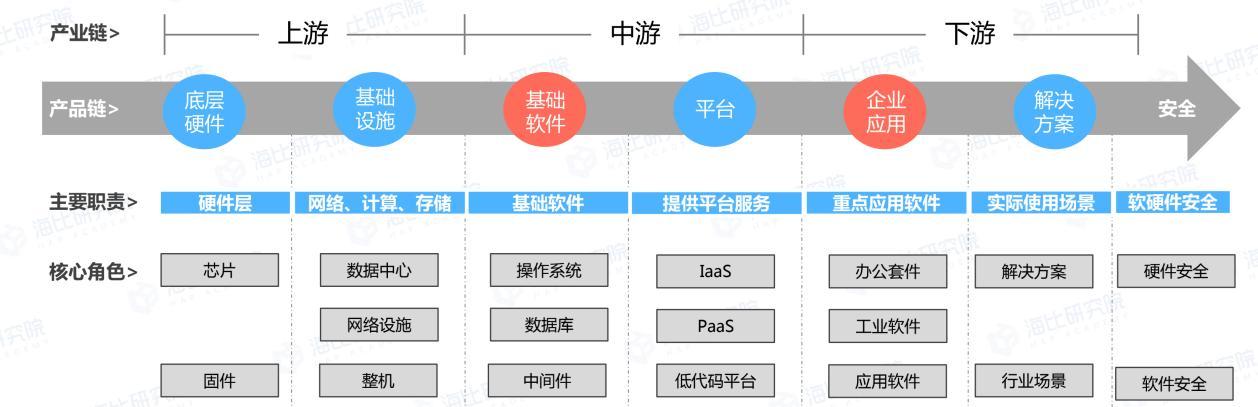

1. Industrial Chain

The ecosystem of the information innovation (Xinchuang) industry is extremely extensive. From the perspective of the industrial chain, it consists of six major segments, mainly divided into:

Upstream: Chips (CPU), storage, PCs/servers, etc.;

Midstream: Operating systems, databases, middleware, etc.;

Downstream: Enterprise applications, solutions, information security, etc.

Figure 1. Panoramic View of the Xinchuang Industry

Data Source: Haibi Research Institute

1.1 Upstream - Underlying Hardware and Infrastructure

It mainly includes terminal equipment, external equipment, communication equipment, computing and storage equipment, etc. CPUs and storage devices are their core components, and the following focuses on the analysis of these two types of core components.

CPU

At present, the mainstream CPU architectures are X86, ARM, RISC-V, MIPS, and Power:

X86 Architecture: Currently occupies the main market share in servers, desktops, and mobile PCs.

ARM Architecture: With the advantages of low power consumption, high efficiency, and a long development history, it firmly dominates the market for mobile terminals such as mobile phones. Currently, it is also the most widely used and mature architecture among non-X86 architectures, with a market share of 43.2%.

RISC-V Architecture: It has a short development history but is more flexible, and has attracted much attention in the Internet of Things (IoT) field. In recent years, it has been focused on and developed due to its open-source nature.

MIPS Architecture: Mainly used in network equipment such as gateways and set-top boxes, with a market share of 9%.

Power Architecture: Minicomputers represented by Power are the core of enterprise IT infrastructure.

Currently, domestic CPU manufacturers have different technical paths:

Hygon: Authorized to use AMD’s 14nm Zen (Zen 1) architecture, it has long-term independent R&D capabilities and a relatively complete ecosystem. However, after being included in the U.S. government’s "Entity List", AMD stated that it would no longer authorize the latest architecture to Hygon. The realization of independent iteration depends on the company’s re-innovation capabilities.

Zhaoxin: Its X86 instruction set is derived from VIA’s patents, not obtained through authorization from Intel or AMD. Its ecosystem is also relatively complete, but it needs to independently develop new instruction sets.

ARM Instruction Set Licensees (represented by Huawei and Phytium): They have long-term independent R&D capabilities and strong product performance, but face potential risks of authorization obstacles.

Self-developed Architecture Manufacturers (represented by Loongson and Sunway): They are leaders in full independent control, with profound accumulation and steady development. Currently, their biggest challenge lies in improving and enriching the ecosystem.

Storage Devices

Storage devices can be classified by form into optical storage (DVD/CD, etc.), magnetic storage (traditional hard drives, floppy disks, etc.), and semiconductor storage. Among them, semiconductor storage is the most widely used and has the largest market scale in the storage field.

Semiconductor storage can be further divided into non-volatile storage (retains data when power is off) and volatile storage (loses data when power is off) based on data retention. Currently, mainstream storage devices in the market include non-volatile storage (NOR Flash, NAND Flash) and volatile storage (DRAM).

At present, China’s NOR Flash chip technology is basically mature, but in the fields of DRAM and NAND Flash chips, there is still a technical gap of more than one generation compared with the international leading level. The manufacturing process of NAND has basically reached its limit, and the industry has begun to shift from 2D to 3D development, which is expected to gradually narrow the gap between domestic technology and that of international giants. Internationally, 64-layer 3D NAND is currently commonly used, while Yangtze Memory Technologies (YMTC) in China has achieved 32-layer 3D NAND, with a gap of only one generation.

1.2 Midstream - Basic Software and Platforms

It mainly includes links such as operating systems, databases, middleware, and cloud computing.

Operating Systems

Currently, mainstream desktop operating systems on the market include Microsoft’s Windows, Apple’s macOS, various Linux distributions, and Google’s Chrome OS; mobile operating systems include Apple’s iOS, Google’s Android, Microsoft’s WP system, etc.; server operating systems are mainly divided into four major categories: Unix, Linux, Windows Server, and Netware; cloud operating systems are also mainly dominated by Windows and Linux.

Due to Linux’s stable performance and open-source characteristics, most domestic operating systems are redeveloped based on Linux.

Databases

A database is a warehouse-like data management system that organizes, stores, and manages data according to data structures. Currently, it is mainly divided into two categories: traditional relational databases and non-relational databases.

Entering the era of Internet Web 2.0 and mobile Internet, many Internet applications exhibit characteristics such as high concurrent reading and writing, massive data processing, and inconsistent data structures. Relational databases cannot well support these scenarios. In contrast, non-relational databases have the characteristics of high concurrent reading and writing, high data availability, massive data storage, and real-time analysis, which can better meet the needs of these applications.

Middleware

Middleware is a hub connecting underlying basic software and upper-layer application services. At present, foreign manufacturers have obvious advantages in products and technologies. Domestic middleware manufacturers focus on developing localization business (mainly for government and enterprises) and commercial business (mainly for small and medium-sized enterprises).

The localization business mainly focuses on narrow-sense middleware (dominated by application servers), and stable migration is the top priority. Since such business has been open-source for a long time, there are basically no problems such as technical barriers or talent shortages.

Cloud Computing

Cloud computing provides users with services such as data storage and software applications through cloud servers. The specific application models of cloud computing mainly include Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS), and Infrastructure-as-a-Service (IaaS).

At present, the most common product application form of cloud operating systems is the combination of "cloud platform system + cloud desktop system". In terms of cloud computing basic products, China has made breakthroughs in EB-level storage system hardware and software technologies, and server system technologies supporting 100-million-level concurrent task processing.

For a cloud operating system to be widely accepted by the market, a rich ecosystem and extensive applications are key conditions. This means that the future market competition among cloud operating system manufacturers will focus on their ability to build ecosystems.

1.3 Downstream - Enterprise Applications and Solutions

Domestic software enterprises are accumulating strength for localization replacement in industry solutions such as ERP, CRM, OA, office software, and MES in the field of application software. They already have the ability to replace foreign software products, and some information platforms have reached the level of basically being able to replace foreign products.

At present, there are a large number of A-share listed companies in application software and vertical industry software, including industry leaders such as Glodon, UFIDA Network, China Software, and Kingsoft Office.

1.4 Cross-Industry Chain - Information Security

Information security refers to the technical and management security protection established and implemented for data processing systems, and has strong universality. It is mainly composed of three major parts: security hardware, security software, and security services.

Information security also has a strong associated attribute—new technologies will bring new application scenarios. With the popularization of cloud computing technology and the continuous improvement of penetration rate, new security protection technologies derived from the new characteristics of cloud computing (such as multi-tenancy and virtualization) are gradually being implemented, such as micro-segmentation in data centers, CWPP (Cloud Workload Protection Platform), CASB (Cloud Access Security Broker) between cloud service providers and consumers, CSPM (Cloud Security Posture Management), and cloud security resource pools based on virtualization technology.

2. Value Chain

Starting from various industrial links and comparing the profitability of listed enterprises, the industries with relatively high gross profit margins are middleware, network and information security, CPU, operating systems, and databases. Among them, middleware is a standardized product, so it has obvious economies of scale and low marginal cost. Its gross profit margin is generally over 90%, and its net profit margin exceeds 40%.

Table 1. Industry Gross Profit Margin Level

Meanwhile, considering the China-U.S. trade war and information security factors, China has long been in a passive position in the IT industry. Therefore, it is urgent to address the "chokepoint" technology issues in China, which are mainly concentrated in the mid-upstream segments of the information innovation (Xinchuang) industry, such as CPUs, storage devices, and operating systems. Based on surveys and interviews with upstream and downstream enterprises, it is found that CPUs, operating systems, and storage devices have higher premium capacity, industry barriers, and industrial added value. As a result, the R&D, design, and production of these segments will generate greater value and have a more far-reaching impact.

3. Cost Structure

Taking the complete machine products of the 706th Institute of the Second Academy (of China Aerospace Science and Industry Corporation) as an example, the main costs of Xinchuang complete machines and system integration products include material costs, outsourcing costs, test costs, and R&D costs.

The material costs of domestic computer products mainly come from material procurement, and the currently procured materials are divided into five categories:

Core components such as processors and bridge chips;

Specialized components such as hardware encryption chips, TCM chips, SoC cards, and three-in-one modules;

Various general-purpose components, including USB controller chips, network controller chips, SATA controller chips, power management chips, as well as diodes, triodes, resistors, capacitors, inductors, etc.;

Peripherals and electromechanical equipment, including memory, fiber optic network cards, RAID cards, optical drives, ATX power supplies, solid-state drives (SSDs), mechanical hard drives (HDDs), keyboards, mice, monitors, and chassis;

Software, including operating systems, BIOS firmware, configuration management software, identity authentication software, host audit software, three-in-one software, and application software (such as WPS Office, 360 Antivirus, and OFD reading software).

Table 1. Product Cost Analysis (Excluding Software)

Chapter 4 Investment Analysis

Huawei: It mainly focuses on the Kunpeng processor and gathers external upstream and downstream enterprises to form the Kunpeng Xinchuang ecosystem.

China Electronics Corporation (CEC) and China Electronics Technology Group Corporation (CETC): Both are state-owned sole proprietorship enterprises directly managed by the central government. They focus on combining self-built ecosystems with strategic investment/cooperation to build a stable proprietary ecosystem.

CEC has China’s most complete independent and advanced industrial chain, covering chips, operating systems, middleware, databases, secure complete machines, and application systems. Its key subsidiaries include China Great Wall [000066.SZ] and China Software [600536.SH]; it has also invested in Qi’anxin [688561.SH] to deploy in the information security field.

CETC is a major force in China’s military electronics, a national team in the cyber information industry, and a national strategic scientific and technological force. It holds a leading technical position in the military electronics and cyber information fields. It controls Westone Information [002268.SZ] and NSFocus [300369.SZ], and indirectly holds shares in Renmin University Jincang and Kingdee Tianyan (delisted) through its subsidiary Taiji Computer [002368.SZ].

Analysis by Specific Product Segments

CPU Segment

Globally, the X86 architecture represented by Intel currently holds the major market share in servers, desktops, and mobile PCs. Key participants in China’s CPU industry include Kunpeng, Loongson, Zhaoxin, Phytium, Hygon, Sunway, and HiSilicon. Among them, Kunpeng’s production capacity cannot be guaranteed due to U.S. sanctions. At present, Phytium has the highest market share, but since Phytium was sanctioned by the U.S. in April 2021, its specific production capacity remains to be monitored.

Operating System Segment

The global PC operating system market is dominated by Microsoft’s Windows series and Apple’s macOS. Data from Baidu Statistics Traffic Research Institute shows that as of December 2020, Windows accounted for 89.79% of China’s desktop operating system market, while macOS held a 6.22% share. Currently, China’s independently developed PC operating systems are mainly Kylin Software’s Galaxy Kylin, China Standard Software’s Kylin, and UnionTech Software’s UOS. Among them, Kylin Operating System occupies a leading position, ranking first in China’s Linux market and holding over 90% of the market share of domestic operating systems in the party, government, and national defense office fields.

Storage Segment

The global DRAM and NAND markets have a high degree of concentration. According to data from China Flash Market, in 2020, Samsung, SK Hynix, and Micron accounted for 95% of the DRAM market; while Samsung, Kioxia, Western Digital, Micron, SK Hynix, and Intel held approximately 99% of the NAND market. The storage chip industry is technology-intensive. China’s storage chip industry started late and lacks accumulated technical experience. Domestic manufacturers such as Yangtze Memory Technologies (YMTC) and Changxin Memory Technologies (CXMT) are still striving to catch up and narrow the gap, while Fujian Jinhua is trapped in U.S. lawsuits and sanctions.

Database Segment

Overseas giants still hold the largest market share in China’s database market. However, with the advancement of cloud computing trends and localization processes, the living and growth space for domestic manufacturers is gradually expanding. Major participants in the domestic market include:

Overseas giants: Oracle, Microsoft, IBM, AWS;

Domestic public cloud vendors: Alibaba Cloud, Tencent Cloud;

Equipment manufacturers: Huawei, ZTE;

Traditional domestic database vendors (the "Big Four"): Dameng Database (Wuhan), Kingbase (Renmin University), Gbase (Nankai University, delisted), Shenzhou General;

Emerging database vendors: SequoiaDB, PingCAP, Transwarp.

Currently, the domestic civil market is dominated by Alibaba Cloud, Tencent Cloud, and Huawei Cloud; the four traditional domestic vendors (Dameng, Kingbase, Gbase, Shenzhou General) are mainly applied in the party, government, and military markets. Overall, although the total market size of the database segment is expected to reach 17.3 billion yuan by 2023, the overall market space for the party, government, and military sectors is limited, and the current market structure has been formed, leaving few investment opportunities. In the later stage, attention can be paid to two enterprises: Wuhan Dameng Database and Renmin University Kingbase.

Middleware Segment

Middleware is one of the three major basic software categories, alongside operating systems and databases. From the perspective of competition pattern:

The first echelon in China’s middleware market (in terms of market share) remains IBM and Oracle, which together account for 51% of the market.

The second echelon consists of five domestic vendors: Orient Software [300379.SZ], Primeton Information [688118.SH], Borland [688058.SH], China Create Middleware, and Kingdee Tianyan (delisted), with a combined market share of 15%.

Overall, although the middleware segment has a high gross profit margin, it has limited market space, scattered competition, and a number of listed companies, resulting in few investment opportunities.

Network and Information Security Segment

Currently, China’s information security industry has low concentration and a scattered competitive pattern. Leading enterprises include Qihoo 360 (delisted from U.S. stock market), Sangfor [300454.SZ], Venustech [002439.SZ], Qi’anxin [688561.SH], NSFocus [300369.SZ], Topsec [002212.SZ], and H3C.

With the development and expansion of cloud computing, Internet vendors have become important players in the network information security field. Among them, Alibaba and Tencent participate in the security market competition through overall business synergy to enhance the competitiveness of their cloud computing businesses. Since the proposal of the Xinchuang industry in 2019, state-owned capital has also entered the information security field, further concentrating the market competition pattern on leading vendors:

SDIC Intelligent invested in Meiya Pico, holding a 15.79% stake and becoming its actual controller;

China Electronics invested in Qi’anxin [688561.SH], holding a 22.58% stake and becoming its second largest shareholder;

CETC invested in NSFocus, becoming its largest shareholder.

Overall, the information security segment already has a number of listed companies, and the entry of multiple state-owned capital entities has led to relatively high overall valuations, leaving few current investment opportunities. In the later stage, continuous attention can be paid to segmented tracks to find valuable targets.

Cloud Computing Segment

At present, mainstream domestic cloud operating system vendors such as Alibaba, Huawei, H3C, and Kylin SecurIT have begun to layout ecological strategies. They have launched comprehensive compatibility and adaptation work covering chips, complete machines, operating systems, databases, middleware, and various application software, and are committed to building a sound enterprise cloud migration ecosystem. Specifically, they expand upward to SaaS (enterprise applications), adapt downward to hardware servers and domestic chips, and integrate horizontally with other leading enterprise software products to accelerate the improvement of the localized cloud ecosystem. Currently, Alibaba Cloud, China Telecom Tianyi Cloud, and Tencent Cloud rank among the top three in the public cloud market.

Downstream Application Segment

In terms of penetration rate, the Xinchuang industry has the highest penetration in the party, government, and finance sectors, and the lowest in the hospital sector. According to statistics from third-party institutions on the industry distribution of Xinchuang enterprises under the national "2+8" system, the degree of industry penetration can be roughly divided into three echelons:

First echelon: Party and government institutions, finance (highest penetration);

Second echelon: Telecommunications, transportation, electric power, petroleum, aerospace;

Third echelon: Education, hospitals (lowest penetration).

This is because under policy guidance, the party and government sectors took the lead in localization; while in the industrial sector, the finance field has a high degree of digitalization, making it easier for Xinchuang penetration.

From the perspective of supply and demand:

On the supply side, leading enterprises such as Phytium, Huawei, Kylin Software, UnionTech Software, and Kingsoft Office [688111.SH] have emerged in the upstream of the Xinchuang industry, and agglomeration effects have been formed in the downstream.

From the perspective of provincial procurement, there are currently two models: centralized procurement and integrator-led procurement, and system integrators will become important beneficiaries.

From the product segment perspective, operating systems, office software, and PCs are the first segments to achieve large-scale adoption, among which PCs are expected to be the first to break through the 10-billion-yuan market scale.

Chapter 5 Analysis of Investment Opportunities in Core Segments of the Xinchuang Industry

Overall, different from the traditional information technology industry, the Xinchuang industry places greater emphasis on the construction of an ecosystem. In the Xinchuang industry, the CPU is the "heart" and the operating system is the "soul". The core logic of the overall Xinchuang solution lies in forming a localized ecosystem centered on CPUs and operating systems, and systematically ensuring that the entire localized information technology system is producible, usable, controllable, and secure.

Domestic Xinchuang industry solutions mainly focus on the ARM+Linux system: domestic manufacturers can obtain full authorization for ARM chips, and the Linux system is open-source, enabling domestic Xinchuang industry to achieve full control over the R&D and iteration of the entire system.

Combined with an analysis of market scale, competition pattern, and technical status, CPUs, operating systems, and storage devices are currently the core segments of the Xinchuang industry with the highest added value.

1. CPU

1.1 Major Industry Participants

Table 8. Overview of Major Participants in China’s CPU Product Market

1.2 Target Company - Tianjin Phytium

2. Operating Systems

2.1 Major Industry Participants

2.2 Target - Kirin Software

Table 13. Financing Status of Kirin Software

2.3 Target Company - UnionTech Software

Table 14. Enterprise Information of UnionTech Software

Table 15. Financing Status of UnionTech Software

3. Storage

3.1 Major Industry Participants

Table 16. Overview of Major Domestic Storage Device Participants

3.2 Target Company - Changxin Memory Technologies (CXMT)

Table 18. Financing Status of Innotron Memory Co., Ltd.

3.1 Target Company - Yangtze Memory Technologies Co., Ltd. (YMTC)

Table 20. Financing Status of Yangtze Memory Technologies Co., Ltd. (YMTC)

Table 21. Analysis of Competitive Advantages of Complete Machine Manufacturers

Table 22. Competition Status of System Integrators

Data Source: Qianzhan Industry Research Institute

Aisino Corporation mainly engages in software integration business, which has relatively low technological content. In the emerging technology sectors of system integration such as cloud computing, big data, artificial intelligence and blockchain, there is a certain gap between Aisino Corporation and other software integration vendors like China National Software Co., Ltd. and CSSC.

Chapter 6 Conclusion

Table 23. Sorting of Unlisted Companies Among Top 100 Xinchuang Enterprises

Data Source: Joint Survey by Deben Consulting, eNet Research Institute, and Internet Weekly (October 2021)

Through the sorting out of industrial tracks, we have established channel resources, organized information on industry associations and exhibitions, and accumulated expert resources in the information technology industry, laying a foundation for the subsequent research on segmented tracks of Information Innovation (Xinchuang). The relevant lists are as follows:

Table 24. Xinchuang-related Competent Authorities and Industry Associations

Table 25. Information Innovation (Xinchuang) Industry Exchange Conferences