In-depth Analysis of Investment Opportunities in the Silicon Carbide Industry Chain

In 1824, a Swedish scientist accidentally discovered silicon carbide during an experiment on artificial diamond synthesis. In 1885, chemist Acheson produced silicon carbide crystals at high temperatures by heating a mixture of quartz sand and carbon. In 1959, Dutch scientists proposed a method for growing single crystals through sublimation. Later, the successful attempt of the step-controlled epitaxy method significantly reduced the epitaxial defects of silicon carbide, and Wolfspeed established the first commercial production line for silicon carbide. In 2018, Tesla became the first automaker in the industry to adopt silicon carbide modules. Infineon, STMicroelectronics, Rohm and other companies have successively invested in the commercialization of silicon carbide devices.

Compared with traditional silicon materials, silicon carbide materials have a wider bandgap, higher breakdown electric field, faster saturated electron velocity and better thermal conductivity, which means silicon carbide is more suitable for applications in high-voltage, high-frequency and high-energy fields.

Table 1 Performance Comparison of Different Semiconductor Materials

The silicon carbide industry chain can be divided into crystal growth, epitaxy, device and application segments. The crystal growth segment includes crystal growth equipment enterprises, crystal growth processing enterprises and substrate material enterprises; the epitaxy segment includes epitaxy equipment enterprises and epitaxy manufacturing enterprises; the device segment includes process equipment enterprises, wafer foundry enterprises, chip design enterprises and IDM (Integrated Device Manufacturing) enterprises with both design and manufacturing capabilities. The application segment is mainly composed of module enterprises that provide downstream application scenarios in automotive, wind power, photovoltaic and energy storage fields.

Table 2 Analysis of Silicon Carbide Industry Chain

There are three main methods for crystal growth: Physical Vapor Transport (PVT), High-Temperature Chemical Vapor Deposition (HTCVD) and Liquid Phase Epitaxy (LPE). Among them, the PVT method is the mainstream method for commercial growth of silicon carbide substrates at this stage. The difficulties of the PVT method are as follows:

(1) Temperature control;

(2) Impurity control: There are many types of silicon carbide crystal structures, but only a few of them are the materials required for substrates, making impurity control difficult;

(3) Slow growth rate: It takes about 7 days to grow a silicon carbide ingot with a thickness of about 2 cm using the mainstream PVT method;

(4) Low yield: Compared with silicon-based materials, silicon carbide substrates have higher process difficulty and lower preparation efficiency.

The localization rate of crystal growth equipment is high, and domestic enterprises such as Jingsheng Co., Ltd., NAURA Technology Group and Jingsheng Mechanical & Electrical Co., Ltd. occupy major market shares. The investment opportunity lies in furnace equipment developed for liquid phase method or HTCVD technology, which can solve the problems of yield or efficiency.

From the perspective of differences in electrochemical properties, silicon carbide substrates can be divided into conductive type and semi-insulating type. Semi-insulating silicon carbide substrates + gallium nitride epitaxy are mainly used to manufacture radio frequency devices, which are applied in fields such as 5G communications; conductive silicon carbide substrates + silicon carbide epitaxy are mainly used to manufacture power devices, which are applied in fields such as new energy vehicles. Physical Vapor Transport (PVT) is the most mature preparation method. The main technical challenge of the HTCVD method is the control of deposition temperature. The main technical challenge of the LPE method is the balance between growth rate and crystal quality.

Large-size substrates can effectively reduce costs and have become an industry trend. At present, the mainstream sizes of silicon carbide substrates are 4 inches/6 inches, among which semi-insulating silicon carbide substrates are mainly 4 which semi-insulating silicon carbide substrates are mainly 4 inches, and conductive silicon carbide substrates are mainly 6 inches. Large sizes can reduce the cost per chip. When the substrate size is expanded from 6 inches to 8 inches, the number of chips can be increased by 75%. The investment opportunity lies in new technologies that improve yield/efficiency.

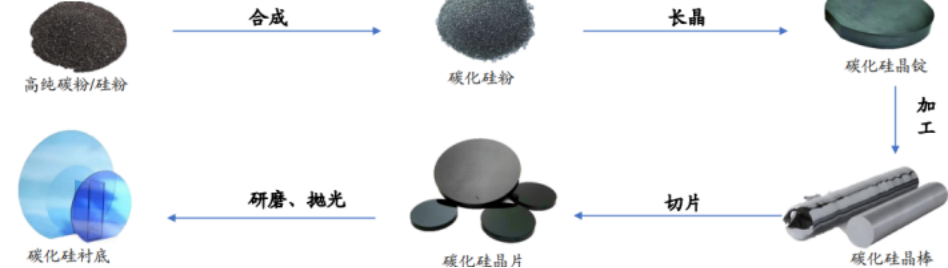

Figure 1 Silicon Carbide Substrate Growth Process

The processing precision of silicon carbide substrates directly affects the performance of devices silicon carbide substrates directly affects the performance of devices, requiring the surface of silicon carbide wafers to be ultra-smooth, defect-free and damage-free. Wire saw cutting is the mainstream technology. Cutting technologies mainly include traditional sawing, wire saw cutting, laser cutting, cold separation and electrical discharge machining slicing. Among them, traditional sawing (such as inner circle saw blades, diamond band saws) has large kerf and high material loss, which is not suitable for silicon carbide crystal cutting; wire saw cutting has mature technology, high wafer output rate, fast speed and low cost, and is the mainstream cutting technology; laser cutting products are in the downstream customer verification stage; cold separation is in the technical verification stage. In the future, diamond wire cutting and laser cutting are expected to replace mortar wire as the mainstream technologies, and attention should be paid to the progress of technology/customer verification of domestic laser cutting enterprises.

The vapor-phase homoepitaxy of silicon carbide is generally carried out at a high temperature above 1500°C. However, due to sublimation, the temperature generally cannot exceed 1800°C, resulting in a low growth rate. Liquid phase epitaxy has a lower temperature and higher rate, but lower output. The technical routes of silicon carbide epitaxy include LPE horizontal CVD, Nuflare vertical CVD and Aixtron planetary CVD. The investment opportunity lies in equipment enterprises that can meet the cost reduction and efficiency improvement needs of large-size substrates.

Silicon carbide epitaxy requires strict defect control and has high process difficulty. Silicon carbide epitaxy will replicate the crystal structure of the substrate, so the epitaxial layer defects include defects from the substrate (such as microtubes, threading screw dislocations (TSD), threading edge dislocations (TED), basal plane dislocations (BPD)), as well as dislocations and macro-defects during the growth process (such as particles, triangular defects, carrot defects/comet-like defects, shallow pits, grown stacking faults). Triangular defects are fatal defects. Epitaxy can be divided into:

(1) Homoepitaxy: Growing silicon carbide on conductive silicon carbide substrates, which is often used in low-power devices/radio frequency devices/optoelectronic devices;

(2) Heteroepitaxy: Growing gallium nitride on semi-insulating silicon carbide substrates, which is often used in high-power devices.

The investment opportunity in epitaxy lies in enterprises with advantages in process technology or cost management.

The technical difficulties of equipment in the device process segment are mainly reflected in the following three aspects:

(1) Ion implantation and annealing activation process: Due to the characteristics of silicon carbide materials, doping during device preparation can only be achieved by ion implantation, and high-energy particle implantation is required. However, high-energy ion implantation will damage the lattice structure of the material itself, requiring subsequent high-temperature annealing for recovery. Due to the characteristics of silicon carbide materials, the annealing temperature is as high as about 1600°C. At such a high temperature, how to ensure the surface roughness of the wafer while achieving a high ion activation rate and a relatively accurate P-region shape is a difficulty;

(2) The silicon carbide trench MOS etching process requires high temperature, and currently there are insufficient domestic models with high-temperature etching capabilities;

(3) Silicon carbide planar MOS needs to improve channel mobility, and currently the core equipment (gate oxide furnace) can only be provided by Toyo Cross (Japan) and CT Company (Germany).

The investment opportunity in process segment equipment lies in equipment manufacturers that can solve the problems of high temperature, high energy and high-intensity etching.

At this stage, upstream epitaxy and substrate manufacturers have significantly expanded production capacity. Upstream substrate manufacturers have further expanded their epitaxy business, while downstream packaging manufacturers have expanded their device manufacturing business. International leading silicon carbide enterprises such as Cree and Infineon all adopt the IDM model. Considering economies of scale, costs and referring to the business models of international giants, the silicon carbide device industry will definitely adopt the IDM model in the future. When investing in device enterprises, the focus should be on the technical indicators of silicon carbide MOS products of device enterprises, the downstream customer groups in automotive, wind power, photovoltaic and energy storage fields, the main driving role of new energy vehicles in the future, and the progress of self-built production lines.

New energy vehicles have two major concerns: driving range and charging convenience. Range anxiety has been alleviated through battery iteration, and the cruising range can now reach 500 km. Charging anxiety is addressed by increasing the charging voltage to improve charging power, and the 800V high-voltage platform solves the charging anxiety. At the Guangzhou Auto Show in November 2023, domestic manufacturers launched 35 models with 800V high-voltage platforms. Silicon carbide MOSFETs have irreplaceable advantages in 800V fast charging. When the voltage increases, the conduction loss and switching loss of silicon-based IGBTs increase significantly. The increased cost and reduced efficiency greatly reduce the actual economy of the 800V platform. Therefore, in the 800V voltage platform, enterprises are more inclined to choose the high-frequency and low-loss silicon carbide MOSFET solution. It is expected that the global sales of new energy vehicles will be close to 20 million units by 2025, with China contributing 50%, and the demand for 6-inch silicon carbide in China will be close to 3 million wafers.

It is expected that by 2025, the scale of newly added silicon carbide devices in the global charging pile market will be nearly 7.4 billion yuan. Due to the application in high-power scenarios, silicon carbide devices have become consumables.

At present, silicon-based IGBTs are mainly used in photovoltaic inverters of photovoltaic equipment. In the future, silicon carbide devices are expected to replace silicon-based IGBTs. Photovoltaic inverters have two basic functions:

(1) Convert DC power to AC power and connect it to the grid;

(2) Improve and optimize the energy conversion efficiency of the photovoltaic system. Therefore, the high-energy efficiency characteristics of silicon carbide devices are very suitable for the above requirements and are expected to be applied at an accelerated pace.

With the expansion of downstream scenarios such as automotive, charging, photovoltaic and energy storage, focus on module and application enterprises with unique business models, and the core is their ability to reduce costs rapidly.

Figure 2 Downstream Application Scenarios of Silicon Carbide

Source: Zhong Hao, Investment Department V

Review: Xue Yao

Release: You Yi